Перед тим як пропонувати агресивну фіскальну консолідацію з метою збалансування українського бюджету, необхідно подумати про те, чи готова Україна до падіння ВВП ще на 5-10%. Розумна макроекономічна політика полягає в утриманні рівня державних видатків, підвищенні ефективності державних видатків, покращенні збору податків та рівня сплати податків, залученні позик із зовнішніх джерел з метою покриття тимчасового фіскального дефіциту.

Швидко наближається 2016 рік, і численні спостерігачі все більше цікавляться тим, як в наступному році буде виглядати державний бюджет України. Міністерство фінансів планує невдовзі оприлюднити проект бюджету та новий Податковий кодекс. Дискусія в суспільстві зосередилася на тому, наскільки великими повинні бути державні видатки та доходи, а отже, яким повинен бути дефіцит бюджету. Запропонований парламентом проект, вірогідно, передбачає величезний дефіцит, принаймні в короткостроковій перспективі, тому що очікувана детінізація економіки не може здійснитися за один рік.

Враховуючи обмежені фіскальні можливості українського уряду, а також нинішню відсутність доступу до позик на міжнародних ринках капіталу, дехто робить висновок, що прийняття збалансованого бюджету (з безжальним скороченням державних видатків) було би розумним рішенням. Більше того, для того, щоб продовжити співпрацю з МВФ, який наразі є основним джерелом зовнішнього фінансування державного сектору, Україні слід утримувати дефіцит свого бюджету в рамках, визначених програмою співпраці з МВФ. Також існують розрахунки, що пропонують уряду знизити відношення державних видатків до ВВП на вісім процентних пунктів.

Чи виправдані такі дії з макроекономічної точки зору?

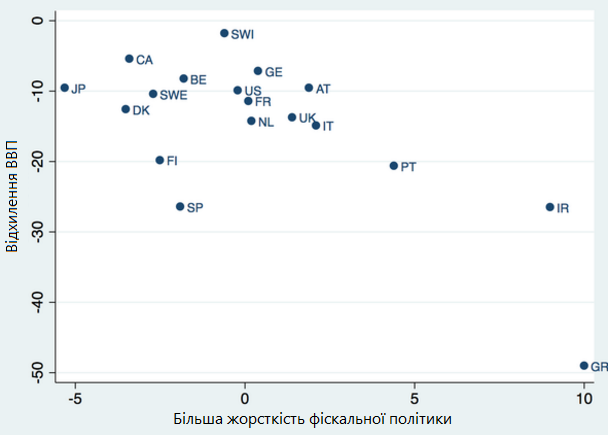

Існують вагомі докази того, що фіскальна консолідація в умовах слабкої економіки є самовбивчою. Механіка процесу проста: скорочення державних видатків знижує ВВП, що призводить до зменшення податкових надходжень, а це в свою чергу призводить до подальшого скорочення державних видатків. Грецька економіка є яскравим прикладом того, як жорстка економія бюджетних коштів в занепадаючій економіці призвела до краху, небаченого з часів Великої депресії. Але випадок Греції не єдиний, і цей урок стосується також інших держав. В нещодавній замітці Пол Кругман продемонстрував очевидний взаємозв’язок між економічними результатами та жорсткістю фіскальної політики. Навіть якщо не враховувати Грецію, проявляється чітка закономірність: більший масштаб фіскальної консолідації пов’язаний з більшим падінням економіки. Можна було би сподіватись на те, що пройшло вже достатньо часу для того, щоб зробити висновки з помилок інших країн, так щоб в теперішній та майбутній політиці уникнути їх.

Джерело: Paul Krugman

Але все рівно заклики до негайного скорочення державних витрат продовжують домінувати в суспільній дискусії. Це приголомшує, враховуючи все те, що недавно відбувалось в інших країнах, а також в Україні протягом 2015 року. Зокрема, ще раніше цього року Міжнародний валютний фонд та український уряд погодили фіскальний план, що передбачав фіскальну консолідацію, еквівалентну шести відсоткам від ВВП, схожого із грецьким випадком масштабу. В березні 2015 року МВФ прогнозували падіння ВВП на 6% за підсумками 2015 року. Ймовірно, цей прогноз було зроблено на основі припущення, що фіскальний мультиплікатор дорівнює приблизно одиниці, тобто кожна гривня, на яку знижують державні видатки, веде до зниження ВВП також на одну гривню. Тоді я припустив, що ці розрахунки, ймовірно, виявляться помилковими: мультиплікатор, скоріш за все, є більшим (рівним принаймні 1,5: кожна гривня скорочення державних видатків веде до падіння ВВП на 1,5 гривень), а отже, ВВП, ймовірно, скоротиться більш ніж на 10%. Тепер і МВФ, і уряд, і приватні провидці передбачають падіння ВВП в розмірі від 11 до 12% у 2015 році. Такий прогноз співпадає із прогнозом, зробленим мною раніше цього року, і явно відрізняється від попередніх прогнозів МВФ та інших експертів. Безумовно, це повинно стати тривожним дзвіночком для всіх тих, хто вважає, що фіскальна консолідація вирішить проблеми України в короткостроковій перспективі. Принаймні потрібно серйозно розглянути ідею про те, що суттєве скорочення державних видатків може похитнути з такими труднощами досягнуту макроекономічну стабілізацію в Україні.

Які кроки є розумними? По-перше, я не прихильник того, щоб залишати все без змін. Україна не може дозволити собі втрачати безцінні ресурси внаслідок всіляких недоліків в забезпеченні суспільних благ. Існує величезний невикористаний потенціал для економії державних коштів, який можна реалізувати шляхом боротьби з корупцією, конкурсного суперництва за отримання урядових замовлень, передачі на аутсорсинг державних програм, більшої адресності державних трансфертів тощо.

По-друге, сподівання на те, що радикальне зниження ставок податків буде самоокупним (тобто що економічний ріст буде настільки стрімким, що податкові надходження не впадуть, незважаючи на нижчі податкові ставки) нереалістичні. Нестача податкових надходжень внаслідок таких кроків в короткостроковій перспективі є дуже ймовірним. Зважаючи на обмежений доступ до позик, уряд буде змушений скоротити видатки, таким чином ставлячи під удар макроекономічну стабілізацію. Більш важливе те, що податкову реформу не можна зводити лише до зниження податкових ставок. Як запропонував Іван Міклош, реформа повинна бути всебічною: вона повинна стосуватися податкових ставок, податкової бази, дотримання правил сплати податків та їх адміністрування.

По-третє, Україна не в змозі залучити кошти для покриття дефіциту з внутрішніх джерел, і є очевидним, що Національний банк України не може друкувати гроші з цією метою. Але в міру успішної реструктуризації зовнішнього боргу, утримуваного приватними інвесторами, Україна покращує свій кредитний рейтинг та може з часом відновити доступ до міжнародних ринків капіталу. Складно передбачити, за якою ціною міжнародні інвестори погодяться надавати Україні позики. 7-8% – близько до ставки за реструктурований борг – здається розумною початковою ціною. Хоча це висока в порівнянні з іншими країнами ціна, вона може бути прийнятною, якщо вірити в значне зростання економіки України у наступні роки (а я в це вірю). Якщо приватні ринки не бажають позичати Україні, уряд повинен подвоїти зусилля по залученню коштів від урядів інших країн та організацій-донорів. Справді, мільярд доларів може здаватися величезною сумою в Україні, але це всього лиш маленька частинка бюджетів багатьох західних країн та міжнародних фінансових організацій. Якщо звернути увагу на сьогоднішнє геополітичне значення України, декілька мільярдів доларів – це невелика ціна. Водночас дуже хвилює той факт, що українському уряду не вдається отримати частину із попередньо погоджених коштів від цих донорів через те, що уряд не може здійснити реформи, в яких зацікавлена сама Україна.

Таким чином, перед тим як пропонувати агресивну фіскальну консолідацію з метою збалансування українського бюджету, необхідно подумати про те, чи готова Україна до падіння ВВП ще на 5-10%. Я в цьому сумніваюся. Точка зору, яка вбачає джерело всіх проблем в Україні у фіскальному дефіциті, є помилковою. Макроекономічні теорія та дані чітко свідчать про те, що до того як українська економіка відновить зростання, фіскальний дефіцит є бажаним. Розумна макроекономічна політика полягає в: 1) утриманні рівня державних видатків; 2) підвищенні ефективності державних видатків (таким чином поступово знижуючи розмір державних видатків, якщо цього бажає суспільство); 3) покращенні збору податків та рівня сплати податків; 4) залученні позик із зовнішніх джерел з метою покриття тимчасового фіскального дефіциту.

Тиждень Податкової Реформи

Податкова Реформа — Підсумок Дискусії (Павло Кухта, член Редколегії iМоРе)

Модернізація Податку на Прибуток Стане Драйвером Зростання Економіки (Анатолій Амелін, венчурний інвестор, засновник аналітичного центру «Amelin Strategy»)

Павло Себастьянович: Середній і Малий Бізнес Витіснений з Легального Поля Високими Ставками Податків (Павло Себастьянович, Громадянська платформа «Нова Країна»)

Олег Гетьман: Упущений Один Досить Важливий Момент у Реформуванні ПДВ (Олег Гетьман, економіст, експерт групи Податкова реформа, Реанімаційного пакету реформ)

Володимир Дубровський: 1-2% Додаткових Доходів в Результаті Тиску на Спрощене Оподаткування — це Нереалістичні Цифри (Володимир Дубровський, експерт реанімаційному пакету реформ)

Сергій Кривошеєв: Малий Бізнес не Отримує Податкових Субсидій чи Преференцій (Сергій Кривошеєв, співкоординатор групи «Економіка і підприємництво» Громадянської платформи «Нова Країна»)

Тетяна Прокопчук: Бізнес Вважає, що Необхідно Спростити Процес Адміністрування податків (Тетяна Прокопчук, Віце-президент з питань стратегічного розвитку Американської торговельної палати в Україні)

Роберт Конрад: Податкова Реформа — це не Просто Зміна Законодавства (Роберт Конрад, Дюкський університет)

Анна Дерев’янко: В Нинішній Ситуації «Косметичні» Зміни не Допоможуть (Анна Дерев’янко, виконавчий директор Європейської Бізнес Асоціації)

Михайло Соколов: З Наявним Рівнем Фіскального Навантаження не Варто і Мріяти про економічне Зростання (Михайло Соколов, заступник Голови Всеукраїнської аграрної ради)

Україні Потрібна Радикальна, але Розсудлива Податкова Реформа (Андерс Ослунд, старший науковий співробітник Атлантичної ради США у Вашингтоні і автор книги «Україна: Що пішло не так і як це виправити»)

Олексій Геращенко: Міністерство Фінансів Готує Свої Пропозиції Практично в Закритому Режимі (Олексій Геращенко, економіст, підприємець, викладач фінансів kmbs)

Роман Жарко: Основна Проблема Української Податкової Системи — Практика Використання Фіскального Механізму Досягнення Запланованого Обсягу Податкових Надходжень (Роман Жарко, к.е.н., Менеджер з оподаткування Baker Tilly)

Податкова Реформа в Україні або Як Досягнути Неможливого (Володимир Дубровський, експерт Реанімаційного пакету реформ)

Податкова Реформа Крізь Призму Макроекономічної Стабільності: Погляд НБУ (Дмитро Сологуб, заступник голови Національного банку, Сергій Ніколайчук, директор департаменту монетарної політики та економічного аналізу НБУ)

Податкова Реформа Визначить Майбутнє України (Павло Себастьянович, координатор групи «Податки» ГП «Нова Країна»)

Податкова Реформа Грузії: Урок для України (Олена Білан, головний економіст Dragon Capital, член редакційної колегії VoxUkraine)

Застереження

Автор не є співробітником, не консультує, не володіє акціями та не отримує фінансування від жодної компанії чи організації, яка б мала користь від цієї статті, а також жодним чином з ними не пов’язаний