The painting: "Carousel". Painter: Mykyta Shalenyi. Source: forbes.net.ua

The painting: "Carousel". Painter: Mykyta Shalenyi. Source: forbes.net.ua

"Are we to be blamed for creating such a good and large bank?" asks Igor Kolomoisky, the former co-owner of PrivatBank, which was nationalized at the end of 2016. His voice betrays that he is offended. "If they do not restructure the loans (to related parties) at market rates within six months, they are going to be prosecuted for leading the bank into bankruptcy," Valeriya Hontareva, the Governor of the National Bank of Ukraine, speaks about Igor Kolomoisky and his partner Gennadiy Bogolyubov. She has no doubt that PrivatBank's owners used the billions of hryvnias deposited in their bank to finance their own business. Kolomoisky disagrees and argues that he was robbed of the bank in what he calls Hontareva's vendetta with him.

Rumors about the nationalization of PrivatBank have been around since the summer of 2016. On a Sunday night, December 18, the government announced that the state became the owner of PrivatBank. It was a difficult decision both for the government and the shareholders because as much as half of Ukraine was serviced by the bank.

Who drove PrivatBank into the nationalization? How much is the most technologically advanced bank in the country worth? What court trials are to expect? We have tried to answer these questions by giving the floor to all sides of the conflict.

"It is not me who is in trouble, it's all of us," one of the participants of the process recalls Kolomoisky's joke at one of the many meetings dedicated to the nationalization. Kolomoisky seems to be unperturbed by anything: polite, friendly, amiable, as if he were not an oligarch with large experience in waging corporate wars. Vitaliy Vavryshchuk, Head of the Financial Stability Department at the NBU, says that PrivatBank's employees willingly communicated with the regulator. They submitted all the required information, visited and talked with the NBU employees over the phone. Kateryna Rozhkova, Deputy Governor of NBU in charge of banking supervision, recalls that Kolomoisky himself visited NBU almost every week.

PrivatBank is one of the four banks, that saw their fate decided by stress testing by the NBU. In 2015, the NBU started checking the quality of banks' assets and their ability to withstand risks, e.g. a drastic decrease in the solvency of borrowers in the wake of an economic crisis. According to the NBU's official data, three banks, Khreshchatyk, Fidobank, and Platinum, left the market after stress tests. PrivatBank was lucky to be nationalized.

Checking PrivatBank took several months and was completed only at the beginning of 2016. "We have looked at all borrowers, collateral, the bank's balance sheet in detail," Vavryshchuk says. The results proved to be discouraging. It was estimated than the bank lacked UAH 113 bn. The number rose to UAH 148bn by the end of 2016. At the press conference in December, Hontareva stated: "We are convinced that the nationalization of PrivatBank is the only chance to rescue the financial system. <…> 97% of corporate loans were issued to related parties."

Valeriya Hontareva, head of NBU

What was it exactly that the National Bank of Ukraine did not like in PrivatBank's reports? The answer is the low quality of loans to corporate entities, which amounted to 155 billion UAH. According to the NBU, those were either the Privat Group's companies or small dormant enterprises. BNE IntelliNews wrote about those borrowers in November 2016, claiming that some businesses in the Privat Group, in particular, the agricultural business, borrowed billions from the bank. According to BNE IntelliNews, the bank lent hundreds of millions of hryvnias to UkrNafta, DneprAvia, 1+1 Studio and many small no-name companies.

Vavryshchuk comments while looking at the list of borrowers, published by BNE, "It is impossible to remember them, they were changing constantly: some companies were removed and were immediately replaced by others."

The central banks deemed collateral used for many corporate loans to be insufficient. Therefore, it is not only that loans were issued either to related parties or no-name companies, but also that the collateral was worthless, e.g. in the form of equity rights to the very same shell-companies.

PrivatBank and Kolomoisky himself tried to convince the NBU that the companies with obscure names actually did operate, while the companies that were allegedly related with the Privat Group had nothing to do with it. They still categorically disagree with the NBU's claim that Kolomoisky's partners accounted for 97% of the corporate loan portfolio and that the collateral for those loans was close to worthless.

"We used two kinds of collateral: property claims under the contract and corporate rights," PrivatBank's manager explains under the condition of anonymity. "Moreover, all loan agreements were subject to English law, in case that the collateral would need to be recovered." He does not deny that some of the borrowers were owned by citizens of Cyprus: is there any other way to do business in Ukraine? It is also true that these companies actually did not do any business and did not own any equipment or other property. "You should understand that a company that operates in Ukraine never shows any assets on the books. Otherwise, the tax administration may confiscate it," the former PrivatBank's manager explains.

"Application of English law is very good," agrees Rozhkova. "Yet we were primarily interested in how the borrowers were going to service their debt if they are not engaged in any economic activity and their collateral is worthless".

PrivatBank's former top-manager cites Surkis brothers and Anatoliy Martynov, former owner of "Retal Ukraine", a company that produces PET packaging, as the example of an unrelated party that borrowed heavily from PrivatBank.

The proximity of Igor Surkis to Kolomoisky is obvious. Zaporozhye Ferroalloy Plant, owned by Surkis brothers, is part of the informal ferroalloy holding of Kolomoisky. Igor Surkis is also a co-owner of Studio 1+1 channel. "I would say, our relations with Surkis brothers are friendly, quite close," Henadiy Boholyubov said in his 2012 interview to Forbes.

When it comes to Anatoliy Martynov, it is difficult to establish a direct link with the Privat Group using only publicly available information, yet in 2008, some media wrote that Kolomoisky and Boholyubov partake in the business.

"The Privat Group is actually not a group, as it has no structure and formally related parties," explains Serhiy Budkin, a partner at FinPoint investment-banking company. "It resembles Islam finance. You lend and then receive a share of income."

How does the NBU define "related parties"? In 2015, the NBU has issued Resolution 315 "On the Procedure of Identifying Banks' Related Parties". Related parties include a bank's controllers, owners, management etc (see the complete list in the Law "On Banks and Banking", Article 52). Financial flows between borrowing companies is an important signal of the relation. "We have analyzed all corporate borrowers of PrivatBank. It turned out that many are serviced by and borrow exclusively from PrivatBank. Moreover, they are connected with other companies in the Privat Group or Kolomoisky and Boholyubov financially and commercially. "Such businesses and their owners are automatically classified as related parties," Rozhkova says. She cites A-Bank, owned by Surkis brothers, as an example.

Mikhail Izumski, an entrepreneur and A-Bank's client, confirms, "PrivatBank and A-Bank constantly stressed that the banks were partners, that A-Bank was actually a subsidiary of PrivatBank. A-Bank serviced PrivatBank's accounts. It does not have its own ATMs or terminals, they use those of PrivatBank and have a joint hotline."

However, Zoya Mylovanova, a lawyer and VoxUkraine editor, believes that the NBU could indeed be subjective in defining related parties. "Resolution №315 gives the NBU much discretion. This allows the NBU to use the standards selectively, in relation to PrivatBank as well," she writes in this article. Serhiy Budkin agrees: "The powers of NBU are so broad that in many cases it has the right to define and formulate the criteria of classifying a party as a related one".

If the NBU was merely picking on PrivatBank and the scale of related party lending was actually much smaller, why did the state need to nationalize such a huge bank?

"We grew very fast and the NBU did not like it at all," one of the ex-managers of PrivatBank is convinced. Kolomoisky agrees: "I myself thought that we were sitting on a powder keg as the future of the bank and the economy was so unpredictable." He argues that all that he is guilty of is that there were not enough funds to recapitalize such a large bank.

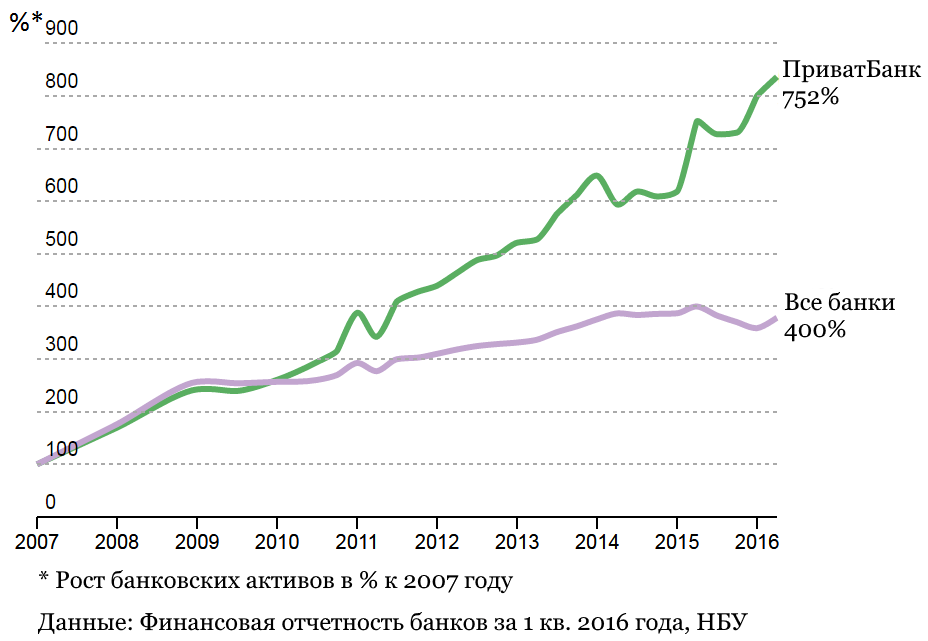

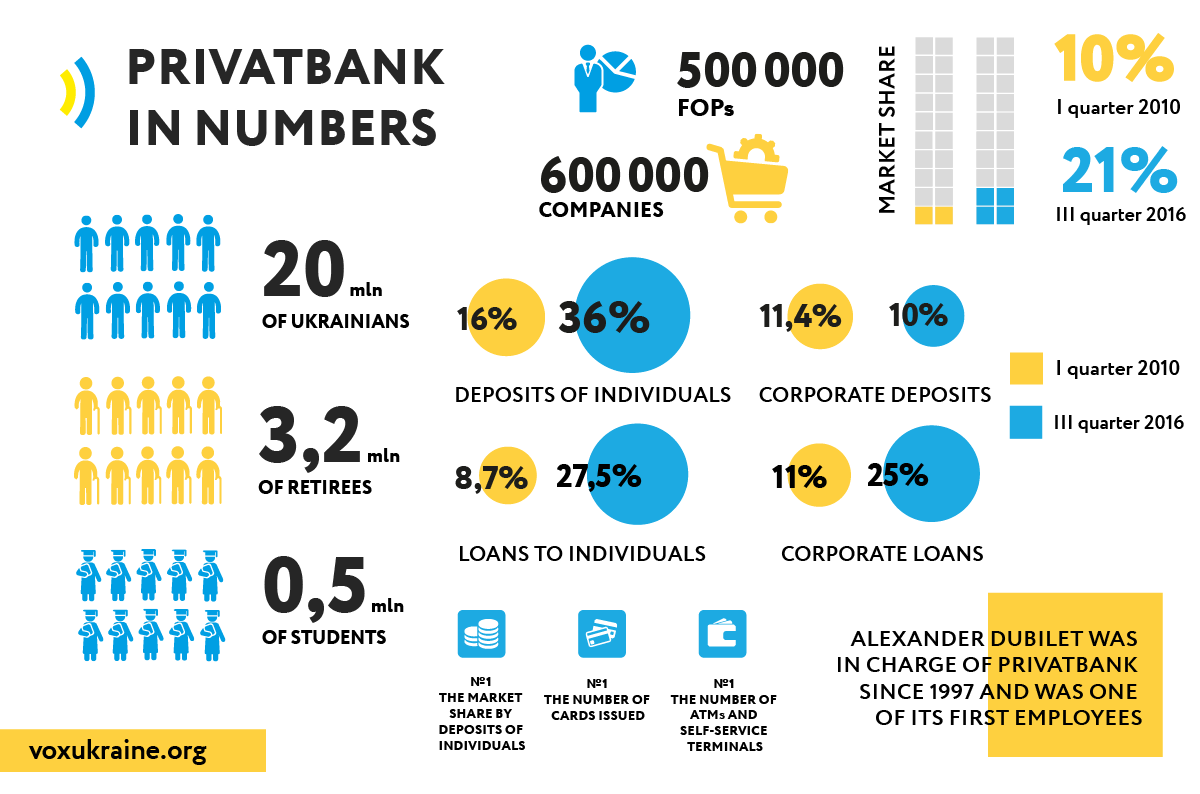

PrivatBank did grow at a groundbreaking speed. In the period from January 2010 to autumn 2016 the amount of cash deposited by individuals increased by 4.5 times, while the deposits by companies increased almost threefold. The bank’s market share by individual deposits increased from 16% to 36%, while the share by corporate loans jumped from 11% to 25% (yet the share by lending to individuals did not change much). PrivatBank was quickly becoming a financial monopoly. "NBU even imposed limits on opening new individual deposits in 2016," says the ex-deputy head of PrivatBank. "We were ready to split the bank and separate its retail banking from the corporate business banking. Yet for some reason, the NBU did not agree."

The NBU provides an alternative explanation of its decision to limit new deposits. According to the NBU, PrivatBank did not fulfill its obligations under the recapitalization program, which it agreed to at the beginning of 2016. There was no talk of splitting the bank. In view of the sheer scale of lending to related parties, the NBU saw only one way out: to restructure the loans. The NBU offered Kolomoisky to transfer the loans to those companies that were engaged in economic activity and had real cash flows. Another option was to unite various business areas in holdings, where some companies only produce and others only trade, yet where cash flows between them are visible. This would have helped increase the quality of borrowers and could partially close the gap in the balance sheet. The next step would involve presenting collateral for loans, e.g. property, equipment, vehicles etc., and covering the rest with capital. "That would be a much smaller amount," Rozhkova says. In fact, the NBU offered Kolomoisky to follow the example of Rinat Akhmetov and Viktor Pinchuk and to restructure his business in the Western manner.

The NBU recognizes that Kolomoisky was not fascinated by the idea. The negotiation took many months and finally, having missed all the deadlines, Privat fulfilled the second condition and presented UAH 31bn worth of collateral in autumn 2016. For instance, according to the NBU, PrivatBank now had Bukovel ski resort, Dnipro-Arena stadium, UIA airplanes, oil bases, offices etc on its balance. The next task was to restructure the loans and to create a transparent structure of Kolomoisky's and Boholyubov's business. According to Rozhkova, they never did that.

Kolomoisky's view is radically different. "At the time when the nationalization was announced, the whole corporate loan portfolio was already restructured in line with the NBU demands. UAH 31bn worth of collateral was put on the balance, while UAH 124bn worth of loans were restructured. The NBU chose suitable companies and the loans were transferred to those companies," claims the former co-owner of the bank.

Ihor Kolomoisky, former shareholder of PrivatBank

Kolomoisky opens an email and reads one of Rozhkova's letters to PrivatBank aloud. According to the letter, in autumn, PrivatBank submitted a plan for restructuring loans issued to companies in the oil and chemical industry. In response, the NBU demanded to present a plan for all corporate loans and set the deadline at October 31, 2016. Kolomoisky argues that the bank did present such a plan. The loan portfolio was then completely modified, exactly as the NBU wanted it.

"Is 75% of the shares of Naftokhimik Prykarpattya a bad collateral?" Kolomoisky is visibly angered. Well, it can hardly be called a good collateral: according to the A-95 consulting company, the only functioning refinery is in Kremechug, while Naftokhimik Prykarpattya does not do that since 2011.

According to Kolomoisky, all accusations of lending to shell-companies and related parties are absurd. "We had a balanced loan portfolio, checked by PricewaterhouseCoopers in line with the IFRS standards," says Kolomoisky. "Is this an insufficient condition?"

It seem that yes, it was not sufficient. "The IFRS definition of a related party does not fully match the related party definition used by the NBU," Zoya Mylovanova explains. Differing definitions are also provided in the Tax Code and in antitrust laws. The reason lies in the difference of the purposes of regulations. The mismatch between the financial reports and the NBU's data may signal that the bank did not comply with the international standards, while the auditor did not check all the sources of information. The NBU confirms that the quality of the auditor's work was not high.

When it comes to restructuring the loan portfolio, Governor of the NBU Valeriya Hontareva is adamant. "They have not done anything. Only under our huge pressure, they fulfilled the first part of the capitalization programme, putting UAH 31bn worth of assets on the books. Yet five days later they removed an asset worth UAH 5.5bn from the balance. They did not present neither the collateral nor acceptable borrowers nor real cash-flows from them," she wrote in reply to VoxUkraine's inquiry.

In 2011, Dmytro Dubilet, together with a colleague, presented their in-house payment service LiqPay at Finnovate Europe conference. "They were the only representatives of Ukrainian business there," the Head of the Board of a large Ukrainian bank recalls. FinTech, or financial technologies, is currently a very popular trend in the world of finance. Many bankers believe that the future belongs not to the banks with their cumbersome infrastructure, but to high technologies. "It is enough to know a phone number to make P2P payments," Dubilet Jr. explains the principles of LiqPay. LiqPay won the prize in the main nomination.

LiqPay is one of the many IT services created at PrivatBank by its legendary IT specialists with Alexander Vityaz, former Head of the E-business Centre, in charge. "We were developing very fast in the fintech," Dmytro Dubilet says. "We always thought that IT was indispensable to any bank."

Corezoid, a cloud operating system, is a much more ambitious project of Vityaz and his team. "Corezoid is an environment, in which it is possible to grow and maintain the digital core of a company. For example, using Corezoid's tools, it is possible to ‘construct’ almost any internet-service within hours," Vityaz explains.

Dmytro Dubilet, former deputy chairman of the IT

"As Bill Gates used to say, ‘Banking will be necessary, while banks will not’," Oleg Gorohovsky wrote on his Facebook page after leaving PrivatBank. In the post, he also spoke about how the employees switched from computers to tablets. The aim was to instruct the bank's clients on the use of the financial structure in a friendly and clear way. "We bought a couple of thousands of iPads and created the single interface for all programs that were used in retail," Dubilet recalls. The project worked for more than two years and led to a breakthrough in the use of Privat24. "It was about then when we started recording the communication of our employees with clients in retail branches. It was very important for us to control speech modules of those who communicated with clients. Their speech was analyzed by machines," Dubilet says. As a result, according to him, the use of various retail products has increased by a third. Not many banks can boast of such innovations.

All these technologies can be hard to swallow for the new PrivatBank's management. "Alexander Dubilet asked Alexander Shlapak (new chairman of PrivatBank’s board – Author’s note) whether he knew what API meant. Shlapak did not," an ex-top-manager of PrivatBank says under the condition of anonymity. "This is surreal. Someone who does not know what API is cannot manage PrivatBank".

It is possible to learn what API is. Yet how to avoid problems with the variety of IT services, created by PrivatBank's team? For instance, Privat24 system is based on Corezoid service. "All the algorithms inside the account are owned by the bank," says Alexander Vytiaz. In simple words, Privat24 is something like a Facebook account or a Google Drive file.

"Corezoid has a contract with PrivatBank. There is a server with Corezoid's copy on PrivatBank' territory, so it is impossible to turn off Privat24from outside," explain Vytiaz. He adds that, as a professional, he outgrew PrivatBank and Ukraine a long time ago. "One organization and one market was not enough to me, therefore I decided to create a global company," says PrivaBank’s former visionary. Corezoid recently signed a contract with Western Union. If the clients found out that the largest Ukraine's bank fell because of Corezoid, they would not like it.

Can Privat24 and PrivatBank's automated banking system, which manages all the processes, be replaced by professional systems from a specialized supplier? "Everything can be replaced. It is only a matter of cost and time that are needed to transfer such a large bank as PrivatBank onto a new platform," speaks VTB Bank’s Chairman Konstantin Vaysman. He transferred PUMB, a Ukrainian bank, as well as Russia's Moscow Credit Bank and RosEvroBank, onto a new ABS. It was never easy.

Dubilet Jr. argues that internal IT-systems of PrivatBank will not be much of a headache as all processes are described and the functions of key programmers are dubbed by other employees. However, according to Vytiaz, the problems with PrivatBank's technologies may emerge elsewhere. "The problem lies not in some mythical buttons or codes, but in the fact that corporate culture and knowledge cannot be moved from one pocket to another and cannot be created overnight. Code is just code. It needs a secret ingredient in the form of the set of skills, namely human capital," argues Vytiaz. He is sorry about, as he predicts it, the gradual degradation of Privat24. "It is impossible to disable PrivatBank by technical means. Yet the very same bureaucrats will do that ideologically, because they don't have a vision and understanding of the system's development," he is sure.

The NBU management believes that possible problems with the IT at Privat is nothing compared to arrears on loans issued to Kolomoisky's and Boholyubov's companies. "Is it true that PrivatBank's shareholders and managers drove it into the bankruptcy? We will know that for sure in 6 months," Rozhkova says. Former shareholders have to restructure the loan portfolio by July 1, 2017. Rozhkova explains that they have to do exactly what the NBU asked them to do earlier, namely to transfer the loans to solvent borrowers and present suitable collateral. If the conditions are met, the loans will not have to be repaid at once. The payments will be spread over a couple of years. If borrowers continue to repay the loans, the bank will continue to work with them.

Former shareholders will not have to inject money, as the NBU and the Ministry of Finance have already or will take care of it. The former lent UAH 25bn worth of refinancing loans to PrivatBank after the announcement of the bank's nationalization. The latter issued UAH 107bn worth of long-term government bonds. PrivatBank will receive funds from the NBU in exchange for those bonds should such a need arise (if the deposits are withdrawn).

Yet, according to Kolomoisky, all loans were already restructured, which relieves him of any financial obligations to PrivatBank. "They claim that I am responsible for something. Why?" he asks. He goes on to explain that it offended him and Bogolyubov the most that PrivatBank's shareholders were presented as criminals.

Bogolyubov suggests that the NBU will be sued by those whom the regulator considered to be related parties and whose money it automatically included in PrivatBank's capital. The sum, according to Bogolyubov, is huge and is equal to UAH 32bn. "UAH 29.4bn," Rozhkova corrects.

"Slightly more than half of the amount was covered by the Eurobonds of PrivatBank worth $555 million (about UAH 15bn). The rest was covered by the deposits and accounts of related parties and individuals, as well as by subordinated debt," Rozhkova says. As of October 1, 2016, PrivatBank's subordinated debt amounted to 7.6 billion UAH. $220 mn out of it were eurobonds. This means that UAH 12.7bn came from related parties.

Bogolyubov is surprised with how selective the NBU's was in deciding whose money to write off and whose not. For instance, Igor Surkis lost several hundreds of millions of dollars. "Interestingly, they did not do anything with the money of his brother Grygoriy Surkis," says Bogolyubov. The savings of Bogolyubov's ex-wife also were used to increase the bank’s capital. "We have been divorced for 11 years," the bank’s former shareholder clarifies. Several more managers of large industrial companies suffered from the nationalization (Bogolyubov names the companies: all of them are partially or fully owned by him and Kolomoisky). According to the registry of court hearings, Surkis family sued National Bank and the Deposit Guarantee Fund at the end of December.

The NBU managers are sure that they made the right decision. Tens of former banks' owners are suing the regulator after it has removed their banks from the market. Valeriya Hontareva is not going to give the former owners of PrivatBank a break. According to the law, they may find themselves in the dock if they refuse to restructure loans. Yet Ukraine's most unpredictable oligarch Igor Kolomoisky assures that he has no complaints against the state. At least, for now.