Today, March 16th 2014, the Crimean puppets of the Russian government ran the “referendum” on whether Crimea should be an independent state or a part of Russia (without an option of staying a part of Ukraine). A staggering 80% of potential “voters” came to the polling stations and a record breaking 95% of “votes” was cast in favor of joining Russia.

This “referendum” was hardly a celebration of democracy and self-determination of nations: voting under the guns of Russian troops, violation of the Ukrainian and international law, made-up lists of voters (the Ukrainian government blocked access to the registry of voters), “pre-answered” ballots, etc. As many observers believe, the next step is that the Russian government will vote to admit Crimea to the Russian Federation thus completing this modern-day Annexation.

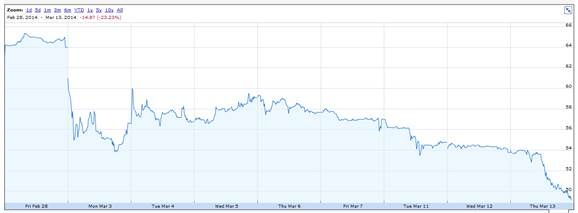

In response to this gross violation of international law, the U.S., EU and the rest of the world are expected to impose wide-ranging sanctions on Russia. While the details of the sanctions are going to be revealed soon, one may expect a significant cost of these sanctions on the Russian economy. Perhaps, the best summary of the omens is the behavior of the stock market in Russia, a forward-looking indicator of Russia’s economic health. As soon as Russia’s Council of the Federation authorized Putin to use troops in Ukraine (March 1, 2014), the stock market fell by 10%. As more information about the response of the Russian and other governments arrives, the stock market has been falling further. The cumulative fall is now about 25%, a shocking amount. Why does the stock market have such a bleak outlook for the Russian economy?

Figure 1. Moscow Stock Exchange Index (MOEX)

To see what determines this pessimism, one can look at the sanctions on Iran imposed in 2010. Both Russia and Iran are heavily dependent on exports of natural gas and oil. These (+ other minerals) account for 70% of Russian exports and 80% of Iranian exports (in 2010). Revenue from exporting these commodities is vital for government revenues and for paying for imports of food, machinery, and other key goods. Economic life in both Russia and Iran is dominated by state-owned companies, which are particularly vulnerable to sanctions. Finally, both countries are dependent on access to global financial markets for obtaining credit and for clearing transactions. In short, the similarities are obvious.

What was the effect of sanctions on the Iranian economy? In short, it was tough.

- Just before the sanctions were imposed, Iran boasted $100 billions in foreign currency reserves. These did not last long, however. Because of the sanctions, about $100 billions of Iran’s money became frozen in foreign banks. For the same reason, only 50% of exchange reserves is accessible. The Russian government is confident that $500 billion in reserves is enough to weather the storm. But Russia’s economy is about 4 times larger than Iran’s economy, and thus $500 billion may be not enough. In the first day of the collapse in the stock market, the Russian central bank had to spend $10 billions in one day to defend the ruble. In the end, the Iranian currency has depreciated by 80%. The Russian ruble has started to depreciate and it keeps falling. The ruble’s value is already at the lowest point on record.

- Because of the sanctions, Iran could not use SWIFT and other payment systems. As a result, Iran had to descent to using barter transactions. Russia is equally dependent on the international financial system and having no access to it would likely raise the cost of doing business in Russia considerably so that the effective price of oil received by Russia is likely to fall.

- Imports in Iran are now dominated by smuggling. While Russia has a longer and more porous border, machinery accounts for 44% of Russian imports which would be hard to smuggle.

- Iran may be losing $50-$60 billion per year in energy investment. Russia depends on know-how from the West to a similar extent and, as a result, exploring Arctic’s oil reserved may stop in the nearest future. The lack of investment can undermine the position of Russia as a key exporter of oil.

- The government in Iran runs a large fiscal deficit ($30 to $50 billion in 2011/2012). The Russian government projected $102/barrel in its 2014 budget, a target that would be hard to achieve with sanctions. A deficit is likely to entail cuts in spending on education, healthcare and other social programs.

- Since Iran’s access to foreign markets was shut down, economy was in recession (output of oil being at the lowest point since 1988), and the fiscal position was weak, the Iranian government had to print money. Not surprisingly, inflation rate is high (38% in 2013, according to the Iranian Central Bank) and getting increasingly hard to control, which is clearly damaging the economy. Many Russians have a memory of high inflation in the early 1990s—hardly a pleasant experience—and the sanctions could bring these memories back to life.

In summary, sanctions similar to those imposed on Iran are likely to inflict deep pain on the Russian economy. Is the Russian invasion into Crimea worth it?

Attention

The author doesn`t work for, consult to, own shares in or receive funding from any company or organization that would benefit from this article, and have no relevant affiliations