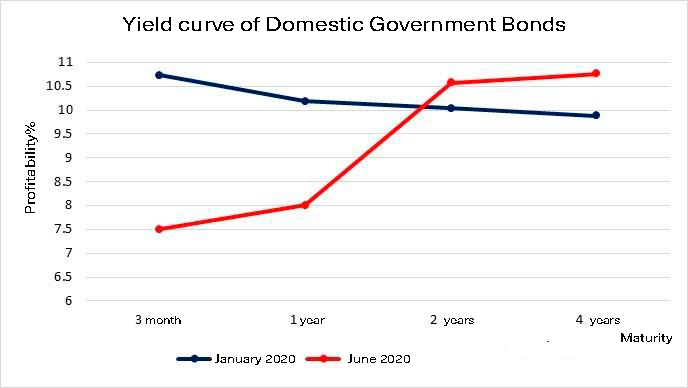

Back in January, the yield curve for Ukrainian bonds had a negative slope. And in June, its slope tilted to positive — that is, now the “long-term” debt is more costly than the “short-term” debt. This change was probably affected by the dynamics of inflation and inflation expectations.

Sovereign debt service is a major part of public expenditure. In 2018, we spent UAH 115.4 billion on servicing domestic and external debt, which is 3.5% of GDP or 12.6% of state budget revenues. This year, Ukraine will spend UAH 141 billion on debt service, which is 12.9% of budget revenues and twice as much as the anti-COVID fund.

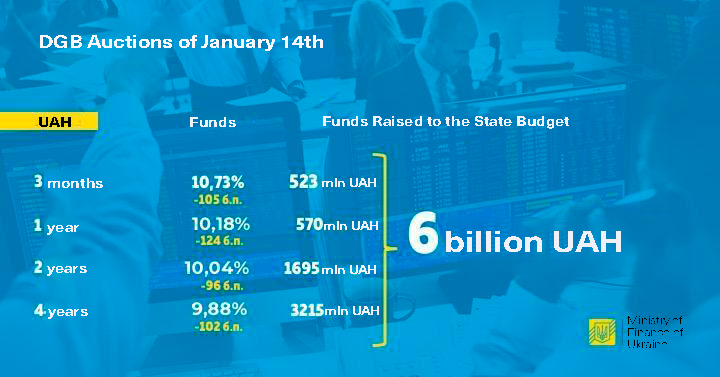

The cost of servicing public debt depends on many factors, including the currency of the loan and the economic situation in the country and the world. A less obvious factor is the maturity, i.e. in how many months or years the government repays the loan. For example, at the auction on July 7, 2020, the Ministry of Finance of Ukraine placed three-month, one-year and two-year bonds in the national currency with yields of 7.24%, 9.5% and 10.2%, respectively. The difference is quite significant.

The dependence of bond yields on maturity is represented by a yield curve. As a rule, the yield curve has a positive slope, meaning that the instruments with a shorter maturity are cheaper than longer instruments. This is due to the fact that in normal times the risk of crises in the short run is lower than in the long run. Therefore, investors invest in longer bonds at higher interest rates.

Another important factor in the yield of hryvnia bonds is inflation and inflation expectations. After all, the higher the inflation, the higher the nominal interest rate should be, so that investors can get the desired real yield (at least not lower than that of foreign currency bonds). Therefore, the higher the inflation, the higher the cost of debt service.

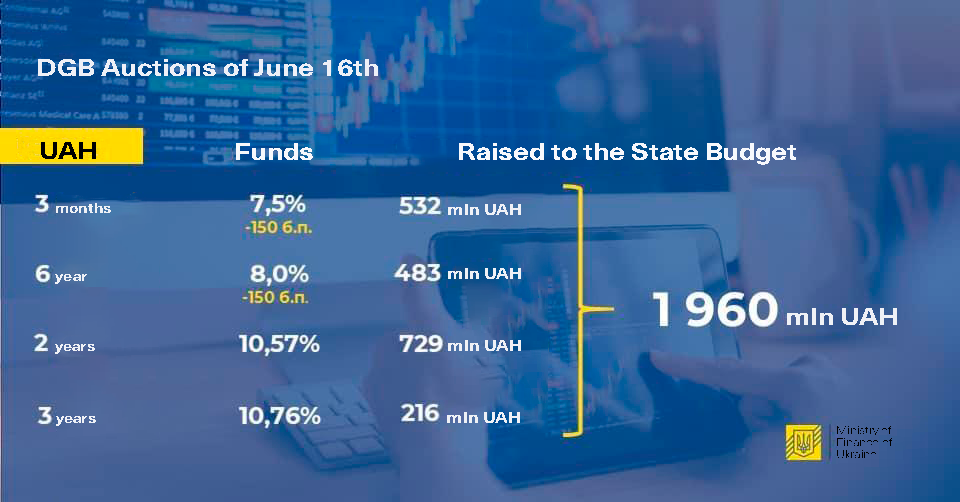

In 2020, the slope of the yield curve changed from negative to positive. As early as January 28, the yield curve had a negative slope, which began to “level off” in February. And in June, the “long” debt was more expensive than the “short” (Fig. 1).

Figure 1. Comparison of hryvnia bond yields at auctions in January and June 2020

Source: Ministry Of Finance

In general, for six months, three-month bonds fell by about 4 percentage points, but the yield on two-year securities increased by about 0.5 percentage points, bonds with maturity of 3-4 years — by 1 percentage point. What caused this behavior of the yield curve?

The reason for such a sharp turn in the yield curve can be the dynamics of inflation and inflation expectations. Inflation decreased from 9.8% in 2018 to 4.1% in 2019 and to 2.5% in the eight months of 2020 (according to the State Statistics Service). Therefore, over the last year there has been a steady decline in the nominal cost of debt service. The negative slope of the hryvnia bond yield curve in 2019 reflected the expectations of investors and creditors to slow inflation and the stability of the hryvnia in the future.

It is clear that such low inflation (2.3% in the first quarter of 2020) is unlikely to last long (the NBU’s inflation target is 5% ± 1%). Therefore, higher yields on longer maturity instruments reflect expectations of higher inflation in the future.

Thus, both inflation and expectations are important factors for the cost of sovereign debt. Changing expectations about inflation or exchange rates in the future have a significant impact on the cost of debt service today. Therefore, the first persons of the state should remember that their words are literally worth millions of dollars — because they affect the expectations of investors, and therefore — the payment of public debt.

Attention

The author doesn`t work for, consult to, own shares in or receive funding from any company or organization that would benefit from this article, and have no relevant affiliations