Ukraine’s agri-food sector is more than just a business—it is a cornerstone of the country’s economic resilience. Despite war, blockades, and global crises, our agribusiness continues to feed the world and sustain the national economy. We reviewed the sector’s performance in 2024 and identified the trends that are carrying over into the early months of 2025.

In December 2024, key players in Ukraine’s agro-industrial sector gathered for the annual Doing Agribusiness in Ukraine conference, traditionally hosted by UCAB in cooperation with the International Finance Corporation (IFC), in partnership with the Ministry of Finance of the Czech Republic and with support from the USAID Economic Resilience Activity. Representatives from the business community, the public sector, and international organizations discussed the expected outcomes for 2024, the major challenges the industry has faced, and the outlook for 2025.

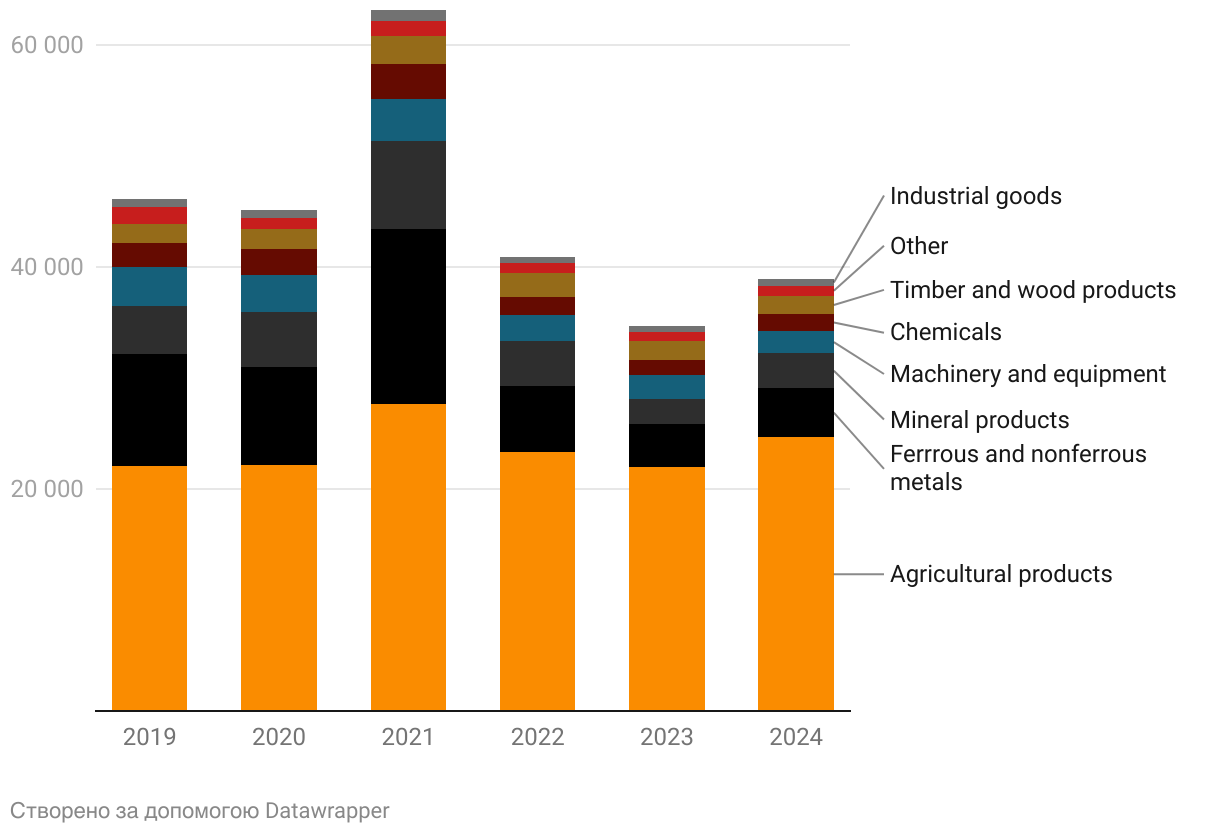

Since the start of Russia’s full-scale invasion of Ukraine, agri-food products have become the country’s leading export category and a major source of foreign currency earnings—significantly outpacing the mining and metals sector, which had traditionally been one of Ukraine’s top export earners. In 2021, agri-food accounted for nearly 44% of foreign currency revenue (Figure 1), but by 2022, its share had grown to 57% and has continued to rise, even as total export volumes declined.

The increase in agri-food exports was partly driven by the sell-off of grain stocks accumulated in previous years. According to expert estimates, carryover stocks stood at around 20 million tons in 2022 and 14 million tons in 2023.

Figure 1. Structure of Ukraine’s foreign currency earnings by export category, 2021–2024 (USD million)

Source: NBU

Note: 2024 data are preliminary.

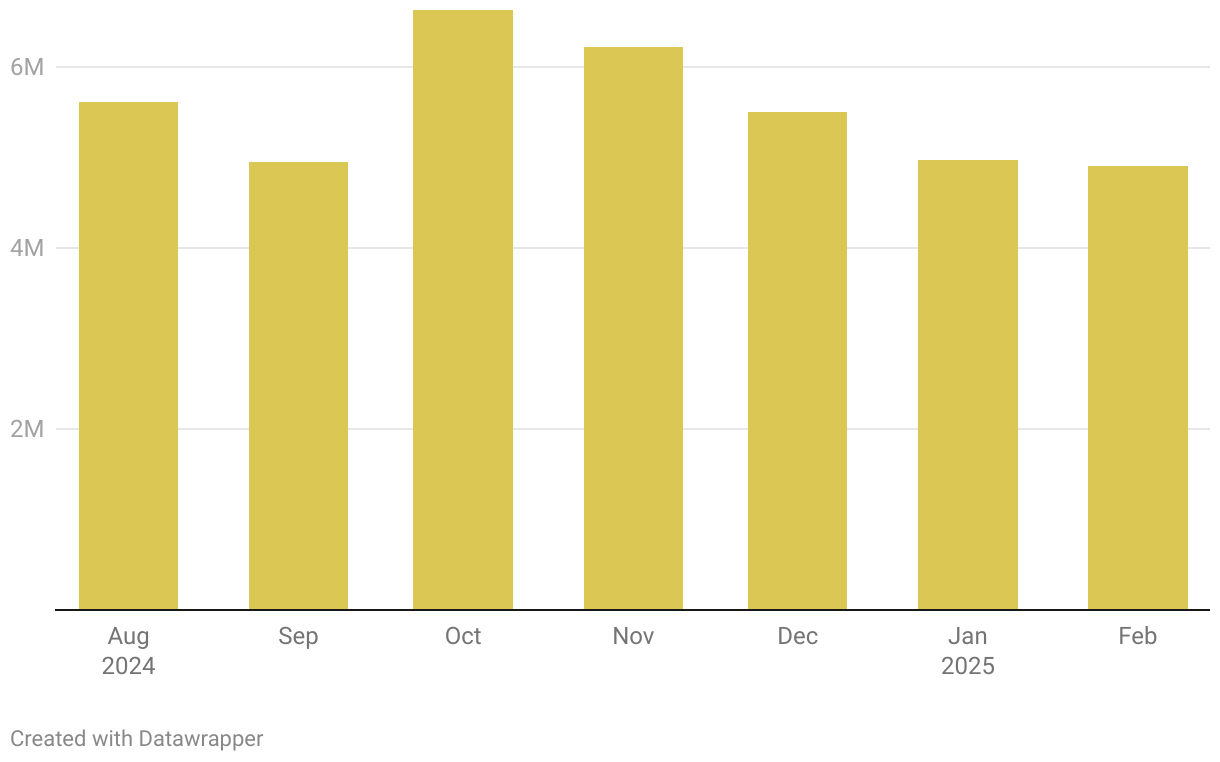

Agri-food exports typically decline during the winter months (Figure 2). For instance, in January 2025, agricultural exports were a quarter lower than in October 2024. Preliminary data for February, particularly for grain and legume crops, also indicate a significant drop in export volumes.

Figure 2. Ukraine’s agri-food export volumes, million tons

Source: Intracen, State Customs Service of Ukraine

The growing share of agri-food in total exports signals an increasing reliance of the national economy on the sector’s performance—and, accordingly, on the risks that affect the stability of agricultural production and exports. Among the key threats cited by experts and market participants are mined farmland, complicated logistics, price volatility, and trade restrictions—challenges that Ukrainian producers have now been grappling with for several years.

Key Challenges

Landmine-contaminated areas

Most of Ukraine’s territory consists of agricultural land—as of early 2020, farmland accounted for 68.5% of the country’s area. In addition to direct occupation (over 18% of Ukraine’s territory as of mid-March 2025, according to DeepState), military activity has left a significant portion of land—up to 30%, especially in the south and east—contaminated with landmines. An area equivalent to two Austrias (1, 2), this contamination poses a serious challenge to both agricultural production and logistics.

According to estimates by the Tony Blair Institute, land contamination by mines and explosive remnants costs Ukraine an estimated USD 11.2 billion in GDP, USD 8.9 billion in export revenues, and USD 1.1 billion in local tax revenues annually compared to 2021 levels.

Landmine contamination is not just a domestic issue for Ukraine—it also heightens risks to global food security. Before the full-scale invasion, Ukraine produced enough agri-food to feed 400 million people around the world each year.

“The reduction in wheat production alone could have fed at least 40 million people worldwide each year,” noted Edmund Clarke, Senior Manager at the Tony Blair Institute for Global Change, speaking at the Doing Agribusiness in Ukraine conference, organized by UCAB together with the International Finance Corporation (IFC), in partnership with the Ministry of Finance of the Czech Republic and with support from the USAID Economic Resilience Activity.

According to World Bank estimates, the total cost of clearing explosive remnants in Ukraine is projected at USD 34.6 billion. This figure is not final and fluctuates depending on the movement of the front line. The cost of demining priority agricultural land alone is estimated at USD 1.5 billion.

Ukraine currently has a program in place to reimburse the costs of humanitarian demining of farmland, allowing agricultural producers to receive 100% compensation from the state budget. This year, approximately UAH 1 billion is expected to be allocated to the program.

Price volatility

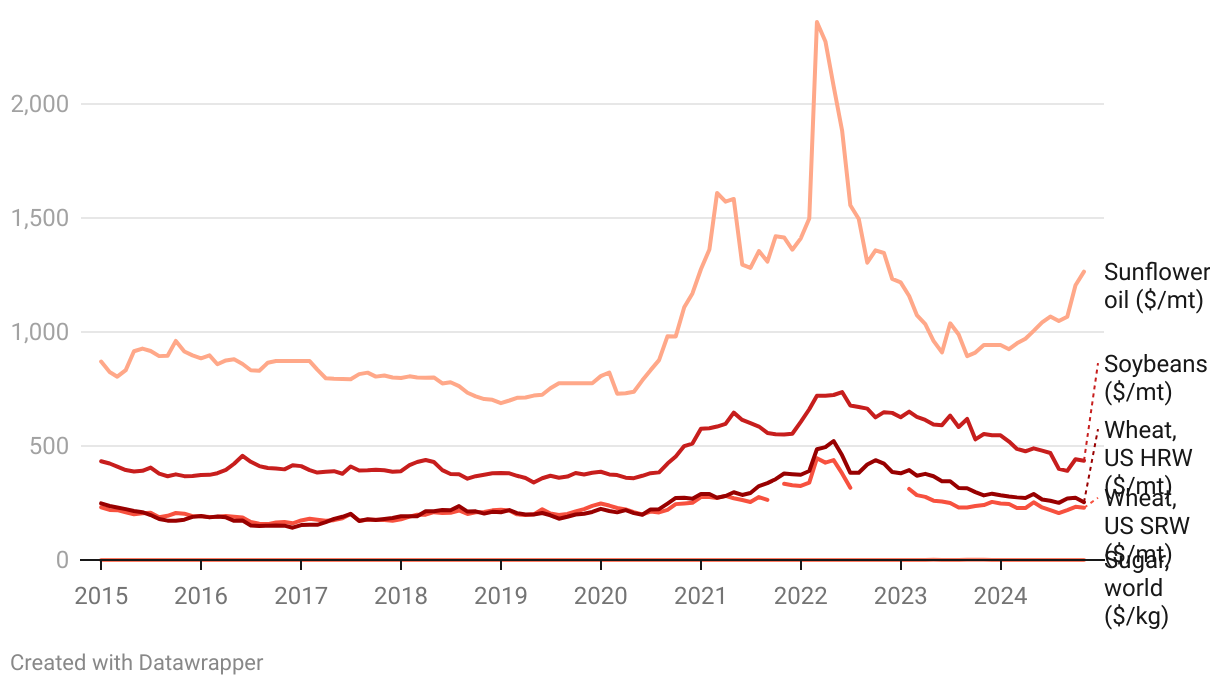

Prices for Ukrainian agricultural products, both on the domestic market and in exports, are influenced by a wide range of factors—including global market conditions (supply and demand), harvest forecasts, weather patterns, military activity, currency fluctuations, and the broader geopolitical environment. As a result, price volatility is significant. Russia’s invasion of Ukraine in 2022 was a major shock that drove global agri-food prices sharply upward (Figure 3), although markets later stabilized. For instance, global prices for sunflower oil—a product in which Ukraine leads the world in export volume—rose in 2024 due to limited supply, while wheat prices dropped to a four-year low as global production increased.

“Last year, the price for corn we sold at the port was USD 125 per t, and our Excel sheet showed that nothing added up. Now, we’re selling at USD 205 per t. […] The biggest challenge for us was the volatility in grain prices and logistics,” said Aivaras Abromavičius, Chairman of the Supervisory Board of the Agroregion Group of Companies, during the conference.

Figure 3. Commodity prices

Source: World Bank

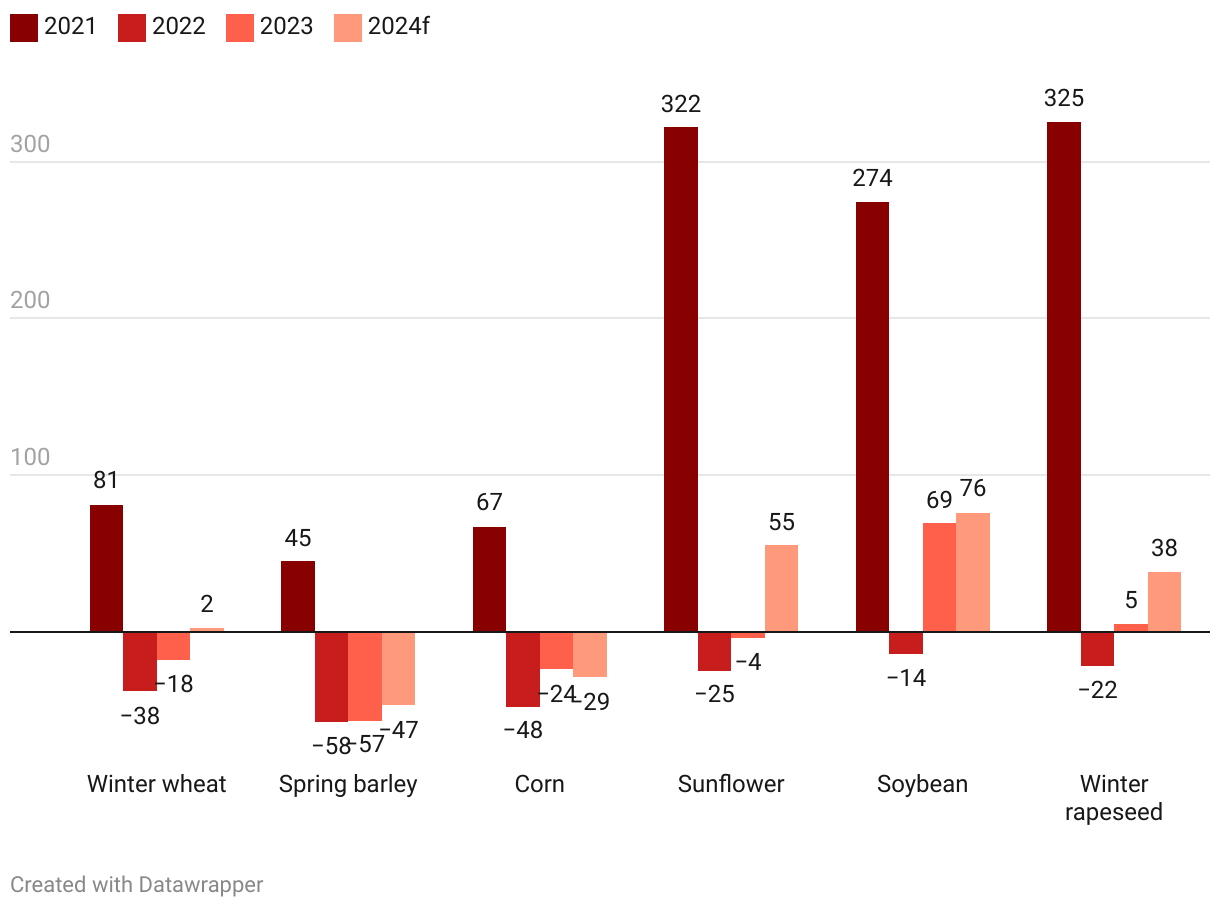

The war places additional strain on Ukrainian businesses, affecting profitability—from direct shelling of farmland, facilities, and grain elevators to shortages of resources and labor, along with higher logistics costs. In 2022, the production of key grain and oilseed crops became unprofitable (Figure 4). Over the course of 2023, the situation improved thanks to the reopening of export routes through Ukrainian seaports, which helped lower logistics costs and drove up domestic procurement prices.

Figure 4. Average profit/loss from production of major grain and oilseed crops in Ukraine, USD/t

Source: Ministry of Agrarian Policy and Food of Ukraine

Note: 2024 figures are projections.

January 2025 began with rising prices for major grain crops, both in Ukraine and abroad. On the one hand, Ukrainian suppliers were shipping gradually, aiming to sell under the most favorable conditions. On the other hand, as of December 1, 2024, the Cabinet of Ministers required the Ministry of Agrarian Policy to set minimum export prices for a designated list of agricultural products. This government measure is aimed at curbing shadow exports and influencing domestic price levels. Experts note that winter is traditionally a “high” season when grain prices, for example, tend to reach their peak.

In its October report, the World Bank projected a 4% decline in global agri-food prices this year, driven by improved growing conditions and increased production in key regions. In Ukraine, the Institute of Agrarian Economics forecasts a rise in agri-food output in 2025, primarily fueled by growth in grain and legume harvests. The USDA’s updated March outlook likewise reflects expectations of increased wheat and corn production.

Logistical challenges

At the outset of the full-scale invasion, Russia blockaded Ukraine’s ports, effectively halting exports through traditional channels. With limited access to Black Sea ports, producers were forced to seek alternative routes and pay premiums for war-related risks. Ukrainian companies redirected exports through European ports, transporting grain by rail or truck. As a result, in 2022, the cost of delivering grain to EU ports reached USD 180–200 per ton—five times higher than pre-war delivery costs to Ukrainian ports. The Grain Deal allowed for a temporary resumption of shipments via Ukrainian ports, leading to a reduction in transport costs. However, Russia ultimately withdrew from the agreement. The situation improved significantly in 2024 thanks to the establishment of the “maritime corridor,” operating under the protection of Ukraine’s Defense Forces since fall 2023 (Figure 5). Still, the continued closure of the Mykolaiv port limits further improvement of the operational environment.

Figure 5. Agricultural exports by logistics channel

Source: Ministry of Agrarian Policy and Food

Note: This includes data for corn, sunflower seeds, soybean oil, wheat, rapeseed, soybeans, meals, and barley.

Ukraine is actively working to expand its export capacity via Danube ports, including Reni, Izmail, and Ust-Dunaisk. However, their throughput remains significantly lower than that of the major Black Sea ports, limiting the country’s overall export potential.

Despite ongoing Russian attacks on Ukrainian ports, the export corridor remains operational and is handling the bulk of grain shipments. Nevertheless, the high level of military threats continues to pose a significant risk to the stability of logistics.

Trade restrictions and European integration

After the start of the full-scale war, the EU fully opened its markets to Ukrainian agri-food products and launched the “Solidarity Lanes”—alternative logistics routes for Ukrainian exporters through neighboring Eastern European countries. On the one hand, this led to a noticeable increase in the presence of Ukrainian goods on local markets in countries such as Poland, Hungary, and Slovakia. Since 2022, European countries have become—and remain—a key destination for Ukrainian exports. This triggered protests from local farmers, who claimed that lower-priced Ukrainian products were “squeezing out” domestic producers. Border blockades on the western frontier have, by some estimates, cost Ukrainian businesses EUR 1.5 billion. On the other hand, a larger share of Ukraine’s exports was transiting through these countries rather than entering their markets—meaning the actual impact was smaller than protestors suggested.

In response, Poland, Hungary, Romania, and other countries temporarily banned the import of Ukrainian grain and other goods, disrupting wartime export routes that had been carefully restructured under challenging conditions. While the European Commission required member states to lift unilateral restrictions, it also imposed temporary conditions on Ukrainian exports—including a ban on importing wheat, corn, rapeseed, and sunflower seeds into the EU until September 2023.

In May 2024, the European Union extended its Autonomous Trade Measures (ATMs) for Ukraine for another year through June 2025. These measures liberalize the export of Ukrainian goods—including agricultural products—to the EU by removing quotas and import duties. However, tariff quotas have effectively been reintroduced for a defined list of goods.

The future of the ATMs beyond June 2025 remains uncertain, and negotiations are ongoing. The Ukrainian government is considering three possible scenarios: continuing the ATMs in their current form, restricting volumes to 2021 levels, which could result in lost export volume and foreign currency earnings, or a compromise approach somewhere in between.

“All players in Ukraine’s agribusiness sector are concerned about what will happen after the trade measures expire in June 2025. As of now, there is no clear framework for their extension,” said Oleksandr Haidu, Chair of the Verkhovna Rada Committee on Agrarian and Land Policy, speaking at the international “Doing Agribusiness in Ukraine” conference.

The issue of Ukrainian product access to the EU remains central to shaping the Common Agricultural Policy—both ahead of Ukraine’s full EU membership and after. On the one hand, Ukraine must continue aligning its legislation, including standards in the agri-food sector, with EU norms and strengthen the capacity of its public institutions. On the other hand, there is a need for a communications campaign within the EU to explain the benefits and synergies of a shared future.

“Ukraine is not a threat to European farmers, but a country that can strengthen the European Union. If we process products together and develop joint logistics routes, the EU can rise from fourth to second place globally in export volume. Together, we will be stronger and more capable,” said Vitalii Koval, Ukraine’s Minister of Agrarian Policy and Food.

Continued domestic and international support for the agricultural sector remains vital to its recovery—not only in terms of improving yields and production volumes but also in restoring export capacity. While some factors, such as weather, are beyond control, others can be actively addressed. Notably, this includes state-funded demining of farmland, as discussed above, and the further development of war risk insurance mechanisms for exporters. A key priority is establishing a shared vision with European countries—so that Ukraine is viewed not as a competitor but as a reliable partner.

Photo: depositphotos.com/ua/

Attention

The author doesn`t work for, consult to, own shares in or receive funding from any company or organization that would benefit from this article, and have no relevant affiliations