Ukrainian lawmakers have taken a step toward revitalizing and invigorating the credit union market, which has stagnated for many years. With the new version of the Law of Ukraine, “On Credit Unions,” replacing the morally outdated law from two decades ago, the proposal is to expand the range of their services, improve the procedures for establishment and exit from the market, and strengthen regulatory oversight and control. This is intended to restore public trust in the institution of credit unions and enhance their resilience and transparency, which is particularly relevant in the perspective of post-war country recovery.

Credit unions have always constituted a small portion of Ukraine’s financial market. Comparing their share in the structure of assets to the most successful year of 2008, it has decreased from 0.6% to less than 0.1%. Their primary activity involves mutual lending among the union’s members using funds accumulated as membership contributions. However, the functionality of credit unions is not limited to lending, as the current law allows them to attract deposits and provide guarantees, essentially acting as sureties for the fulfillment of obligations by the union member debtors to other creditors. The activities of credit unions are not oriented toward profit generation, although this possibility is not ruled out.

They operate alongside banks, partially intersecting in functionality and conditions for providing loans. However, credit unions are largely oriented towards population segments with limited access to banking services (rural areas), those accustomed to such cooperation (older people who had experience with the so-called “mutual aid funds” in the Soviet era), or those who prefer to collaborate with like-minded individuals (such as religious organizations). Additionally, credit unions can bring together citizens who, for various reasons, cannot access appropriate financial services from banks (for instance, retirees who sometimes face limitations in obtaining loans).

The National Bank of Ukraine carries out supervision of the market in accordance with the split law. They are high-risk financial institutions, as they accumulate the financial resources of their members, which can be lost in case of unprofessional actions by the union’s management. Therefore, they require objective, comprehensive, and effective state oversight, clearly defined “rules of the game,” and predictability of their participants’ behavior.

The credit union market in Ukraine

According to the World Council of Credit Unions, the number of credit unions worldwide (considering 118 member countries of the Council) amounted to 87.9 thousand in 2021, with nearly 393.9 million members. The global average penetration rate (the ratio of credit union members to the economically active population) was 12.69%, compared to only 1.21% in Ukraine. Credit unions are much more prevalent in Europe and the USA than in Ukraine. For instance, in 2021, the penetration rate was 61% in the USA, 5.5% in Poland, and 9.5% in Lithuania.

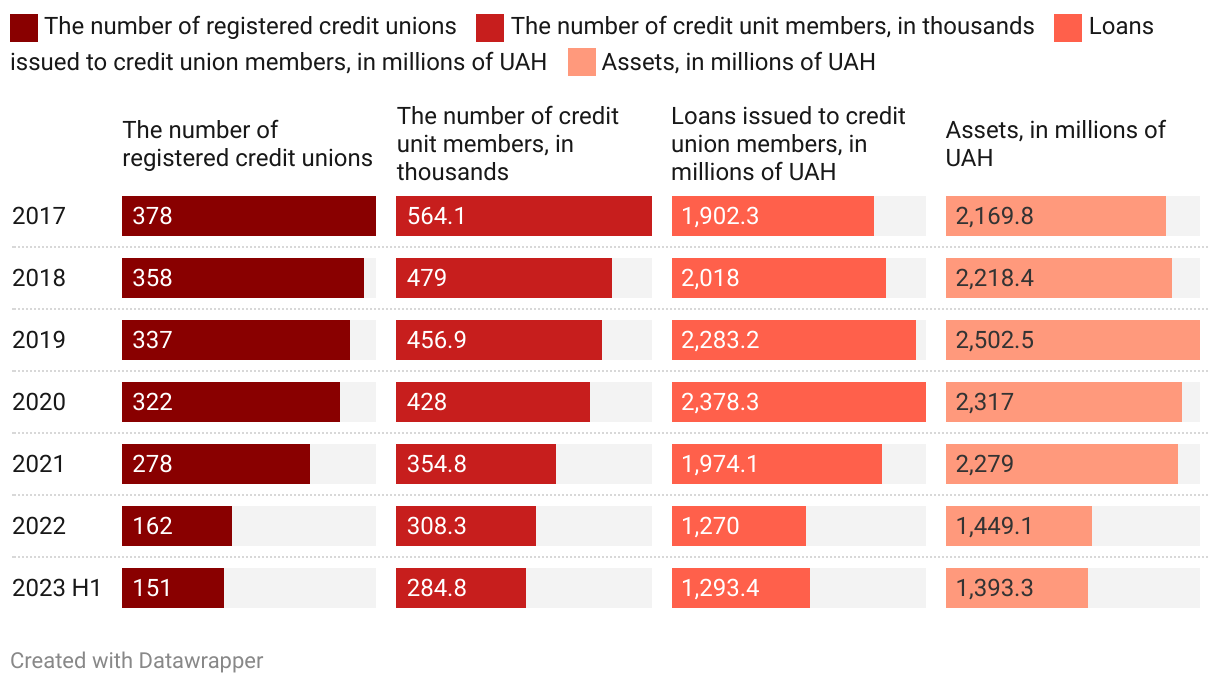

The credit union market has been operating in Ukraine since the restoration of independence, and according to the data from the National Bank of Ukraine, it peaked in 2008, just before the global financial crisis. The market saw a revival in 2010-2013, but Russia’s aggression and the subsequent economic downturn in 2014 had a detrimental impact on the activities of credit unions.

Over the past seven years, the market has continued to stagnate: the number of credit unions, their members, and the size of assets have been decreasing. By the end of H1 2023, the number of credit unions amounted to only 18% of the peak in 2008, and their assets were slightly less than UAH 1.4 billion compared to over UAH 6 billion in 2008.

A sharp decline in the credit union market indicators occurred in 2022 with the onset of Russia’s full-scale invasion (Figure 1). Some unions were forced to suspend or terminate their activities due to the occupation of the territories they operated in, decreased economic activity among the population, and the unpreparedness to work in conditions of operational risks that materialized.

Specifically, in Q1 2022, the volume of new loans decreased by 1.5 times compared to Q1 2021, according to NBU data. The number of entities decreased by 40%, and the remaining volume of loans issued to members of credit unions by the end of 2022 decreased by 36% compared to the end of 2021 (this reduction in loan volume occurred due to the unions exiting the market and a decrease in lending by those that remained). The beginning of the full-scale war also negatively affected the dynamics of bank lending. In particular, the population reduced its demand for credit resources immediately after the invasion, although the magnitude of the reduction was smaller compared to the credit union market. For instance, according to NBU data, the volume of bank loans granted to individuals at the beginning of 2023 was 13% lower compared to the beginning of 2022

Figure 1. Key indicators of the credit union market in Ukraine

Source: NBU

Note: The indicators are provided as of the end of the respective period.

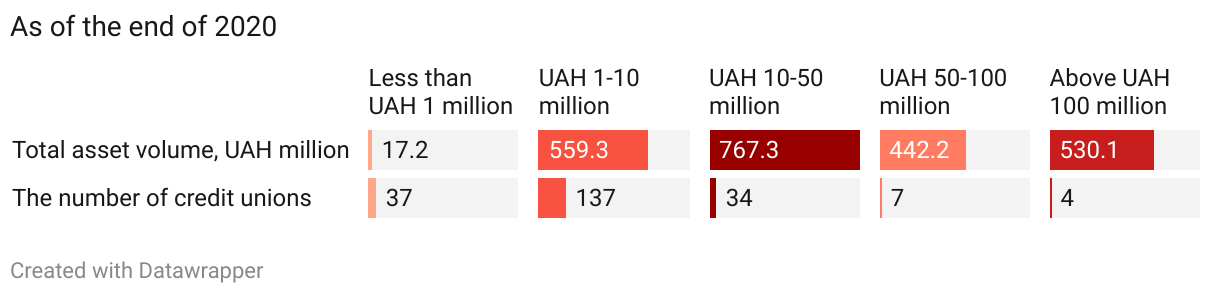

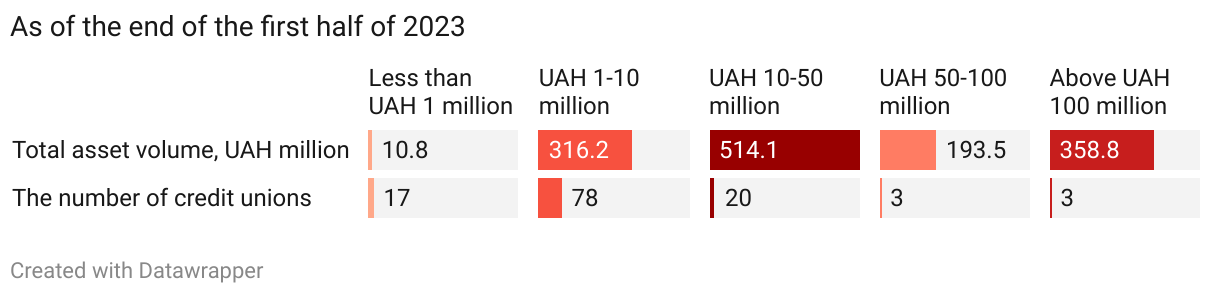

The market structure remains practically unchanged (Figure 2): the majority of unions have assets of less than UAH 10 million (95 unions in 2023), and only three credit unions have assets exceeding UAH 100 million. These three entities were also among the largest in 2020. However, another credit union with assets over UAH 100 million at that time had its license revoked last year due to failure to submit financial reports.

Figure 2. The market concentration of credit unions in Ukraine

Source: NBU

Note: The total number of credit unions may not match the data in Figure 1, as not all of them report their activities.

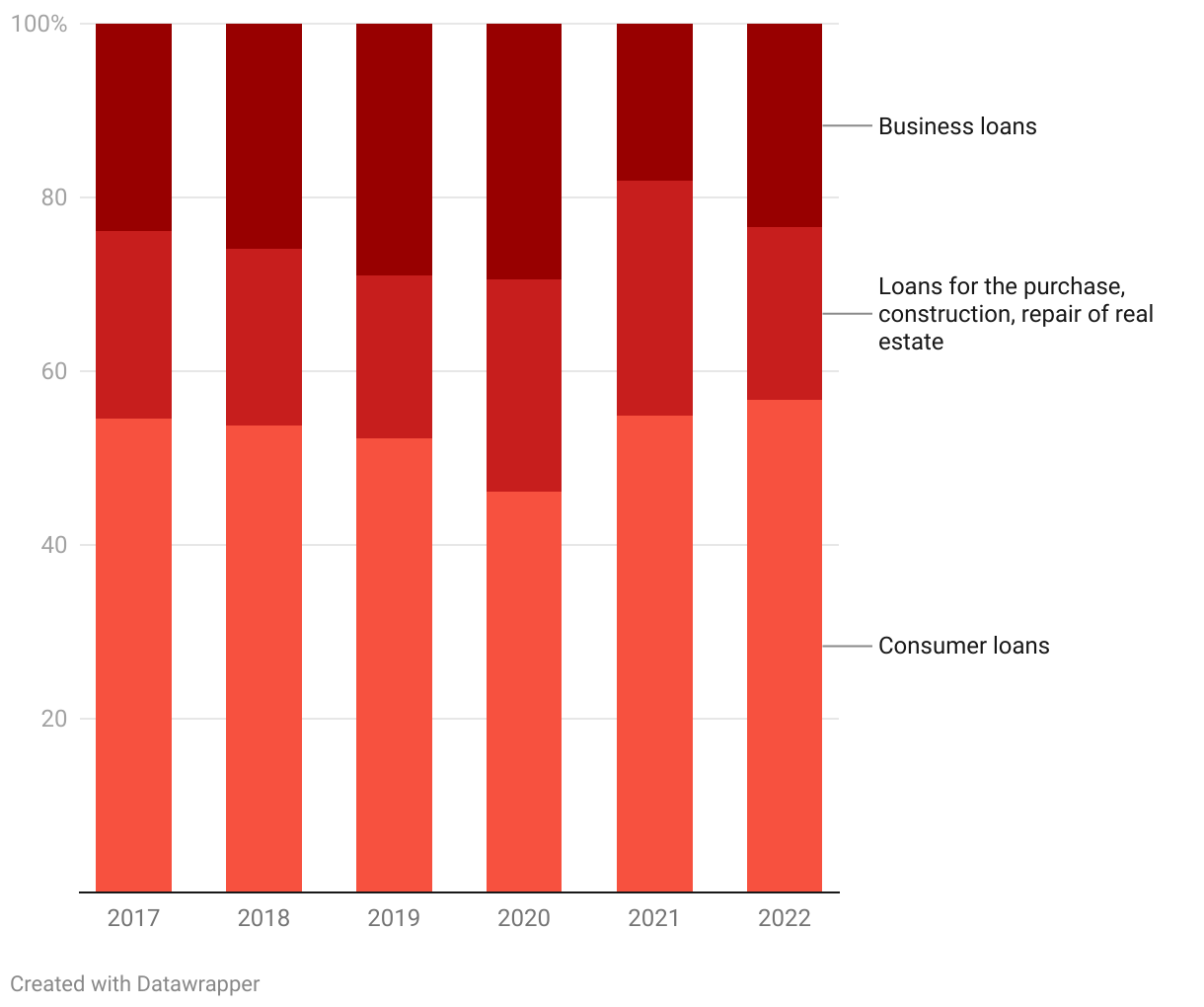

For what purposes do credit unions issue loans? More than half of the volume is consistently consumer loans (Figure 3).

Figure 3. Structure of the principal loan debt amount from credit union members, %

Source: NBU

Currently, the regulation of credit unions is carried out based on a law adopted in 2001. Despite undergoing changes over the course of 20 years, it has become morally outdated and does not take into account modern practices of financial activities, the level of technological advancement, etc

The imperfections in the legal framework, coupled with economic crises, have led to the systematic accumulation of problems in the credit union market. Entities face liquidity shortages and eventually insolvency due to limited sources of capitalization and/or poor corporate governance. Moreover, the clients of credit unions are mainly elderly individuals who are more economically vulnerable. The oversight of credit union activities was based on outdated rules that constrained an adequate assessment of the credit unions’ solvency and the regulator’s ability to respond promptly to actual and potential challenges.

To address these issues, in 2020, the National Bank of Ukraine (NBU) introduced a draft new law; however, Parliament did not approve it. Instead, in 2021, a new parliamentary bill (No. 5125) emerged, adopted in July 2023 after two years of revisions. This legislative proposal takes into account the requirements of the Association Agreement with the EU and harmonizes the legislation in the financial services field.

After being signed by the President on August 30, the law will come into effect the day following its publication. However, its implementation will commence on January 1, 2024.

What changes does the new law envisage?

Changes to the essence and functionality of credit unions

According to the current law, a “credit union is a nonprofit organization founded by individuals, professional associations, their unions on cooperative principles, for the purpose of meeting the needs of its members in mutual crediting and providing financial services through pooled monetary contributions of the members of the credit union.” In the new version of the law, the characteristic of being a nonprofit has been removed from the definition, and it has been clarified that a credit union provides not only financial but also other services as prescribed by the law.

At the same time, as before, only individuals can be founders of credit unions, and their number must be at least 50 individuals.

One of the main innovations is the expansion of the accessibility of credit unions. In addition to individuals, as currently provided, members can now include individual entrepreneurs and a defined list of legal entities. This list comprises agricultural enterprises, cooperatives, primary or local professional associations, religious organizations, associations of co-owners of multi-apartment buildings, and micro-enterprises. These entities can only be members of credit unions created based on territorial criteria (and for micro-enterprises, they must also meet specific criteria).

To become a member of a credit union, individuals and individual entrepreneurs must meet one of the membership criteria: territorial affiliation; common workplace; affiliation with the same labor union or religious organization operating within the territory of the credit union’s registration; education or work at the same educational institution.

For reference, the territorial criterion implies residing in the populated locality (village, town, city), district, or region where the credit union is registered and in all or several adjacent populated localities, districts, or areas.

Additionally, separate branches of credit unions can be established. Depending on the membership criterion, branches can be set up in populated localities where organizations that the credit union is based on (such as labor unions) are present, or branches of enterprises or educational institutions are registered that serve as a common workplace or place of study for the members of the credit unions.

In order to access the financial services of a credit union (e.g., to obtain a consumer loan), an individual must be a union member. The rules for becoming a member are regulated by the law on credit unions and the statute of each union. A potential participant in the union must submit an application for membership, after which the union’s governing bodies decide on their acceptance into the union. Following this, the individual pays the entrance fee and obligatory share contributions (their amounts are determined by each union independently). The first day of membership is considered to be the day of full payment of the obligatory share contribution. After this, the participants can avail themselves of the union’s services.

It is important to clarify that according to the current law, the amount of credit a single union member can obtain cannot exceed 20% of the union’s capital. The volume of deposits made by a participant into deposit accounts (i.e., the union’s obligations to a single member) cannot exceed 10% of the total obligations of the credit union. These limitations are not established in the new law.

The current legislation provides for a limited range of services that credit unions offer to their members. Primarily, this includes lending, attracting deposits, and providing guarantees. The updated law expands the spectrum of financial and other services. Depending on the type of license — simplified or standard — a credit union either provides funds and banking metals on credit or may also attract funds and banking metals as deposits. Upon a separate request, the regulator can include in the license services related to providing guarantees and financial payment services (except for interaction with electronic money). With a separate license, a credit union will also have the right to engage in currency exchange and/or currency transfers without opening an account.

Moreover, legislators have allowed credit unions to engage in other economic activities related to the main activity of providing financial services or necessary for greater accessibility of financial services to their members. This includes placing free funds on deposits in banks, purchasing government securities and bonds of international financial organizations (that are placed in Ukraine), attracting loans from banks and other credit unions, providing loans to such unions, acquiring property and leasing it, and providing consulting and informational services in the field of finance. However, trading and material production are prohibited.

To enhance credit union activity transparency, these organizations are required to have a website.

A separate section of the new Law is dedicated to defining and regulating a united credit union (UCU), founded by at least 20 credit unions on cooperative principles to promote their financial stability and provide financial services to their member credit unions. Unlike “ordinary” unions, a united credit union must be nonprofit. United credit unions will be able to establish a stabilization fund to support the solvency of their entities. In its White Book, the NBU noted that such unions could significantly boost the development of credit unions and increase their solvency level, thus enhancing their reliability. Unlike the banking sector, where there is a Deposit Guarantee Fund for individuals, such an institution does not exist in the credit union market, so these associations potentially could fulfill a stabilizing role.

Changes in corporate governance of credit unions

The new law improves the governance system of credit unions: it outlines general requirements (which were not present before), introduces changes to the procedure for conducting general meetings (e.g., allowing remote meeting sessions via video conferencing), and mandates the establishment of an internal control system (risk management, compliance, internal auditing).

In addition, a procedure for self-assessment of credit union leaders in accordance with the qualification requirements established by the National Bank is introduced. The NBU will approve candidates for positions of leaders of united credit unions and significant credit unions (those that are significant for the market and meet criteria that the NBU has yet to develop) and may also require the termination of the powers of any of the leaders, chief risk manager, compliance manager, chief internal auditor of any union if non-compliance with qualification requirements or inadequate performance of their duties is identified as a result of supervision.

Another innovation is the right of credit unions to outsource functions, specific tasks, and processes within such operations.

Changes in supervision and regulation

The new law simplifies the registration and licensing of credit unions by merging them into a single procedure. Moreover, it allows for changes to the scope of the license – either reducing or expanding the range of services a credit union can provide.

The law defines the procedure for a credit union’s exit from the market – voluntarily (liquidation or reorganization of the credit union) and by a court decision when the NBU classifies the credit union as insolvent or in case of license revocation.

Credit unions will be governed by new requirements regarding the structure of their capital. The regulator will establish prudential standards using differentiated approaches (considering the size, significance of the credit union, and the nature of its operations), conduct supervision using a risk-oriented approach (1, 2, 3), and adhere to the principle of proportionality (balancing public and private interests). As a result of strengthening management and improving regulatory oversight, credit unions are expected to become more reliable and their work more transparent and stable, thereby reducing the likelihood of their bankruptcies and enhancing the protection of union members’ rights.

Conclusions

The changes envisaged by the new law will not be a “silver bullet” or solve all the problems accumulated over decades in the credit union market. However, these steps are meant to lay the foundation for shaping new “rules of the game.” The credit union sector should become more resilient, reliable, and transparent. Moreover, the current crisis is not just a problem but also an opportunity for development that needs to be seized.

In addition to the changes already adopted (at the time of preparing this publication, the law is awaiting the President’s signature), the regulator has plans for the development of non-bank financial services after the war. Specifically, proposals are being developed for the establishment of a guarantee system for credit unions (currently, they are not members of the deposit guarantee system). Credit unions will participate in state and international credit programs aimed at rebuilding sectors of the economy affected by the war, housing reconstruction and development programs, and entrepreneurial development, including agriculture.

With the support of

![]()

Attention

The author doesn`t work for, consult to, own shares in or receive funding from any company or organization that would benefit from this article, and have no relevant affiliations