While currently all eyes are on fiscal policy developments in Ukraine, the monetary and foreign exchange policy also underwent remarkable shifts when the full-scale Russian invasion started last year. The National Bank of Ukraine (NBU) was basically forced overnight to abandon inflation targeting, fix the exchange rate and introduce capital controls. More than 18 months into this war, more and more signs appear that this drastic shift was a prudent one that helped to stabilize the macroeconomic situation.

The international reserves are at an all-time high, there is no pressure on the foreign exchange rate and inflation is in rapid decline. This sweet spot, as well as obligations arising from commitments under the IMF programme has now motivated the NBU to adopt and publicly release a strategy that sketches the long and winding path to an eventual return to pre-war macroeconomic policies. While many risks originating from the ongoing war may potentially delay or stop the move towards liberalisation of capital controls and more FX flexibility, it is nevertheless a step in the right direction.

Background

Ukraine operated successfully an inflation targeting policy as a nominal anchor and a floating exchange rate just until the beginning of Russia’s full-scale invasion on 24 February 2022. However, the massive shock of the full-scale invasion forced the NBU to quickly provide a 180-degree turnaround.

The inflation targeting regime requires an effective transmission mechanism of the policy rate to the real economy. However, Ukraine had to prioritise monetary budget financing – a policy that was prohibited before the introduction of the martial law – over inflation stability as the economy collapsed and international aid was not able to close the fiscal gap in the first months of the full-scale war. Moreover, Russia’s blockade of main export routes strongly weakened the transmission effectiveness. These reasons forced the NBU to return to a fixed exchange rate policy as the nominal anchor for monetary policy instead of inflation targeting to stabilize expectations, with the introduction of heavy capital controls.

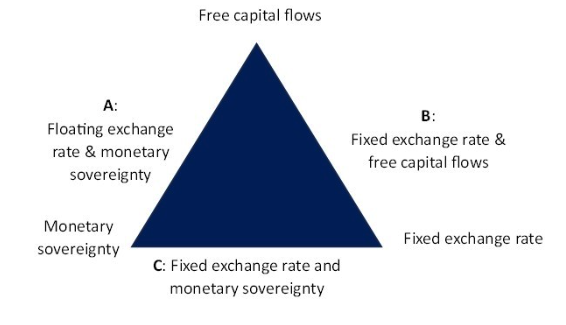

Ukraine has had a prudent track record of adjusting its monetary policy to external shocks. When Russia started its invasion in 2014, the NBU introduced strict capital controls. At the same time, preparatory steps to transit from a fixed exchange rate anchor to the inflation targeting framework were under way. While the inflation targeting policy was put in place in 2016, capital flows were not fully liberalised until 2019. According to macroeconomic theory, central bank policy rate decisions affect capital flows. These flows change the demand for domestic currency. Therefore, a fixed exchange rate regime is compatible with either monetary sovereignty or free capital flows (“monetary policy trilemma”) – figure 1.

Figure 1. The monetary policy trilemma

As a result, a sovereign monetary policy with a fixed exchange rate regime requires capital controls. Ukraine thus had to move from A to C when the full-scale invasion started in 2022.

Was the regime change successful?

Even though there are good reasons to question the role of broad-based capital controls, the regime change was important to calm expectations under extremely high uncertainty and thus contributed to maintaining macroeconomic stability under very adverse circumstances. International reserves remained at sufficient levels even before the large inflows of international aid started to arrive (figure 2).

Figure 2. International reserves and their import coverage

Source: NBU

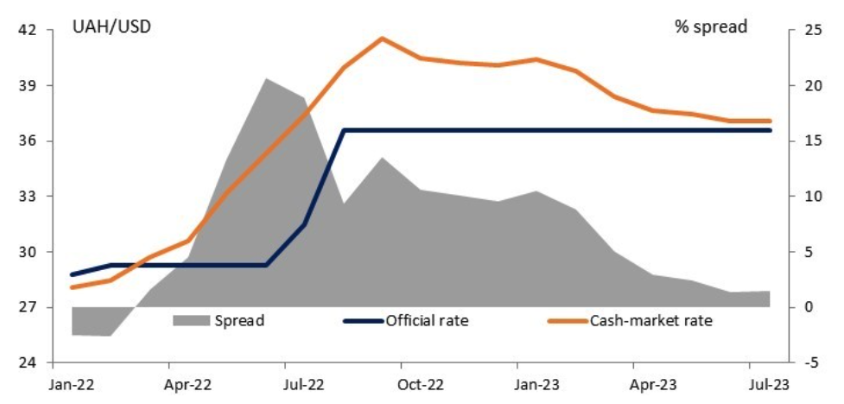

International reserves have never fallen below three months of import coverage. Since July 2022, the situation has improved as Ukraine has been able to export some agri-food products via the sea within the Black Sea Grain Initiative. Furthermore, international aid has come more regularly and on more predictable terms. Currently, international reserves cover more than five months of imports. Similarly, the improved macrofinancial situation can be observed in the development of the spread between the official exchange rate and the cash market one, which basically disappeared (figure 3).

Figure 3. The spread between the official and the cash-market rate

Source: NBU

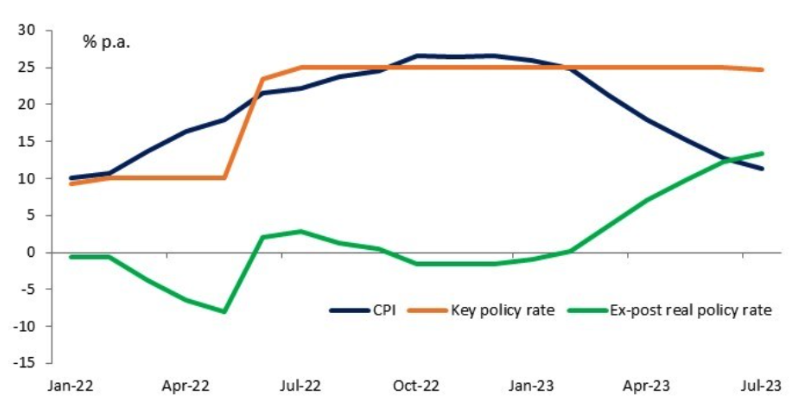

An important step in stabilizing exchange rate expectations and increasing the demand for deposits in UAH was the steep hike of the key policy rate by the NBU in mid-2022. With the end of monetary budget financing – a stop of fiscal dominance over monetary policy – another important step towards normalization was made. Inflation has been on a declining path since then and more recently, the ex-post real key policy rate moved into positive territory (figure 4). And finally, the NBU started an easing cycle at the end of July with a cut of the policy rate to 22% p.a. The baseline assumption is further rate reductions below 20% p.a. later this year.

Figure 4. Inflation and key policy rate

Source: NBU, monthly average key policy rate

Therefore, it is not surprising in the current macrofinancial situation that the NBU signals further steps towards monetary policy normalization to prepare the public for a gradual way back from C to A, i.e. moving back to a floating FX rate regime with free capital flows and the focus on bringing inflation back to target.

The strategy for the long way back

In the framework of structural benchmarks within the current IMF programme (EFF), Ukraine committed to develop a conditions-based strategy to outline the transition to a more flexible exchange rate, easing of capital controls and a return to the inflation targeting policy. This strategy was approved on 29 June and a strategy document was published on 7 July.

Ukraine already implemented a few steps to ease the restrictions. Particularly, foreign investors have been allowed to repatriate coupons on government bonds since April 2023 and in the end of June the NBU eased restrictions for residents to service new external loans as well as for non-bank financial institutions to withdraw domestic and foreign currency from their bank accounts.

This strategy sets up further steps to ease FX restrictions that will continue along a gradual path and will concern trade transactions next. Liberalisation of trade finance, repatriation of coupons on debt obligations as well as household transaction shall follow at later stages in the future. The flexibilisation of the exchange rate regime and the return to inflation targeting will be complemented by keeping a tight monetary policy stance with a positive real policy rate and reintroduced measures to manage liquidity positions in the banking sector.

On the one hand, the current macro-financial situation with a very tiny spread between official and cash market exchange rate, unprecedented high level of international reserves and disinflation show a window of opportunity to restart a gradual flexibilization of the exchange rate regime and a return to inflation targeting (IT). On the other hand, current inflation expectations are strongly impacted by regulatory capped energy tariffs. This regulation is part of the government policy decision-making, and thus exogenous to the National Bank’s monetary policy.

Ukraine’s government and its international partners have to balance fiscal implications of this policy and upside pressure risks to inflation expectations. A gradual return to IT is only possible if inflation expectations are firmly anchored for the purposes of monetary policy. All in all, assuming the current macrofinancial situation remains and the caps to be maintained as the heating season is just a few months ahead, a gradual return to IT is worth considering already this year.

Outlook

Despite the improved situation, which allowed for the release of the strategy, any future step will be taken only after a case-by-case assessment of macroeconomic developments, as uncertainty remains very high. For example, a deteriorating fiscal situation, delayed international aid or a dramatic change of the security situation are key risks that can postpone or stop the NBU’s steps towards implementation of this strategy. Still, the public commitment to move back from macroeconomic management under war conditions back to the pre-war situation is a positive step for Ukraine and its partners. However, international effort to further support Ukraine in ending this war as soon as possible is the most efficient way for improving the macrofinancial conditions.

Attention

The authors do not work for, consult to, own shares in or receive funding from any company or organization that would benefit from this article, and have no relevant affiliations