Recently the international Association of Chartered Certified Accountants (ACCA) released it’s survey’s results claiming that Ukrainian shadow economy comprises almost 46% of the official GDP. The government’s estimation is somewhat lesser – about 35%, still a lot. Whatever the real number is, different players, from the IMF to domestic business and some active citizens are eager to fight shirking from “civil duties” and help to fill the Treasury’s coffers. Unfortunately, there are many illusions that often drive these efforts in wrong, even harmful, directions.

I have already addressed these issues two years ago in the article called “Rampant tax avoidance/Evasion: hunt a big fish first” providing some illustrative figures to demonstrate real relative and absolute scales of different kinds of evasion/avoidance avenues. Recently we (present author together with Vyacheslav Cherkashin, and with kind help of Roman Semko) at the ISET accomplished much more robust analysis of them based on the data from various sources, and our own calculations. Of course, the very nature of this topic implies that there cannot be really “hard” and exact data, thereby possible errors are sometimes comparable to the magnitude of the values. However, these, the best available, estimations still can provide a right order of priorities for “de-shadowing” policies, to the extent the latter are justified at all. Our findings mostly reinforce the conclusions of abovementioned two-years-old article that I would not like to reiterate here, instead recommend a reader to look at the original text.

What is important about “shadow economy”

Before getting to the results of our inquiry a brief explanatory note on how these numbers should be interpreted is needed.

Firstly, the words “budget losses” should be used with caution, since we can more or less reliably calculate only the money that was actually not paid as taxes. However, to be sure, present state of the art should be compared to an imaginable situation in which they would be paid – and it makes a difference, because a real economy always has certain elasticity that can vary from one case to another. Thus, if we state, say, that “the Treasury loses 10 bn. UAH annually due to poor administration of the property tax” – this can be close to the truth, because the immovable property cannot be concealed from taxation: one cannot hide it or avoid paying the tax, otherwise the object will be simply confiscated. But when it comes to the estimates of “losses” from envelope wages and other abuses at the labor market, elasticity cannot be ignored any more, because many of the workplaces in question would never be created if an employer has to pay labor tax in full; yet another part would be less paid and likely left vacant while potential employees migrating abroad. Putting it differently, in the case of labor, unlike property tax, we deal with a market. Thus, estimating the “losses” as just “prices difference” multiplied on the same quantity of output is grave mistake, since at a higher price it cannot be sold at the market in the same amount.

Estimating the “losses” as just “prices difference” multiplied on the same quantity of output is grave mistake, since at a higher price it cannot be sold at the market in the same amount.

Secondly, the “fighters” against shadow economy, especially the auditors and legal professionals, often present it as something intolerable that should be eliminated at any price. From the economic perspective, however, any kind of policies are justified only to the extent that benefits they bring exceed the costs they incur. Such analysis is far from being trivial, because there are many non-fiscal and even non-economical factors involved. For instance, in the example above, on the one hand there is an implicit social cost incurred by tolerance of unlawful behavior of any kind; on the other hand, a real unemployment or labor migration are, arguably, even worst an evil than a “gray” employment due to numerous negative externalities they create. Furthermore, one should take into account that reducing “fiscal losses” means just some re-distribution of already existing value between the broad economy’s sectors; while the cost is, usually, some kind of transactions costs – which means net social losses. Therefore, a proposition alike “the government would be better off spending UAH 1 bn. for cash registers in order to raise additional 1.2 bn. in revenues” would be economically justified – by increasing the social wealth – only if the government can actually spend that money as brilliant as they bring an equivalent of 2.2 bn. in the “value” of public goods to cover social losses.

More generally, “fighting the shadow economy” is dubious goal as such. This is especially true if the fighters suggest the measures that can further deteriorate Ukraine’s unfavorable business climate, further reduce miserable share of small business (and induce market power respectively), and/or increase the corruption opportunities for tax officials. Instead, contraction of the shadow economy should come as a desirable side effect of the liberal fiscal reform that includes reform of the corporate tax, expenditure (thereby, tax) cuts augmented by fiscal maneuver from income taxes towards recurrent property taxation as advised by the OECD, further lowering of the entry barriers for micro business and self-employment, improvements in taxation of natural resources (including land). Most probably, after these reforms and some well-targeted special compliance-increasing measures the shadow economy will spontaneously shrink to the scale that makes further “de-shadowing” efforts unjustified.

After these reforms and some well-targeted special compliance-increasing measures the shadow economy will spontaneously shrink to the scale that makes further “de-shadowing” efforts unjustified.

But how these special measures should be targeted and prioritized? Here one should take into account that Ukrainian version of “shadow economy” is quite peculiar, much different from, say, the classical Hernando de Soto’s description. Not only that the bulk of Ukrainian “shade” is not truly unofficial but a part of operation of legally registered entities, also it is comprised mostly of the large firm’s activities, however strange it may look for the first glance.

This is because, for one thing, there is little problem in registering a firm, especially a sole proprietor, and using the simplified taxation system (STS).that provides for modest unified lump-sum or turnover taxes and no bookkeeping but a sales record (here is the earlier article specially devoted to this topic). Hence, the entry barriers to official sector are generally low except for a few cases where a license is required, as in construction (and here, indeed, a classic kind of informal sector flourishes). For the second thing, among the large firms only few multinationals are transparent public companies, the rest belong to “oligarchs” that due to their embedment in state power can afford misbehaving, including massive tax avoidance and fraud. To complete the picture, Ukrainian economy is overwhelmingly dominated by large and extra-large firms and conglomerates; meanwhile really small business (eligible for STS) constitutes just 7.1% (8.2% with correction for underreporting, see below) of total enterprises’ sector turnover.

There is, however, still quite high totally unofficial sector that increases every time authorities try to curtail the STS so it fails to perform its role as an instrument for “compromise de-shadowing” and sheltering small business from the extortion of corrupt tax inspectors going after officially registered firms. Early 2017 year more than 300 000 sole proprietors cancelled their registration after the law amendment proposed by the Ministry of Social Affairs that required them to pay “minimum social contribution” regardless of whether they actually perform any activity or not; or has it already being paid for them at some other workplace. Before, in 2011, when the Azarov’s Tax Code has largely increased tax liabilities for the STS payers and attempted to eliminate its most important provisions, the losses were even larger: more than two millions of workplaces in small business. Most probably, large part of them moved to the fully unofficial sector and never came back.

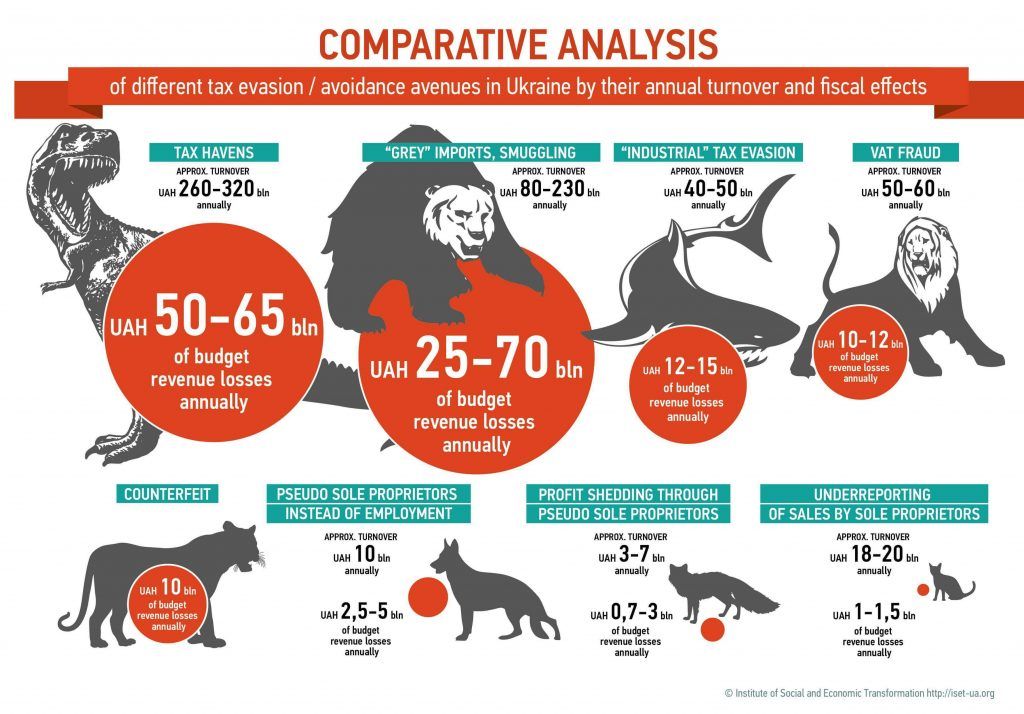

Our study provides quantitative evidences about the real structure of Ukraine’s shadow economy, as opposite to perceived one, which is, in this case, misleading. We managed to inquire the main known avenues that incur conditional fiscal losses totaling about 6-10% of the Ukraine’s official GDP. Given that the share of taxes (including so called social contributions) in the country’s GDP is about 32.5%, this means that violations covered by this study amount for 20-30% of the official GDP, which constitutes 50-80% of the “shadow’s” share. The rest should be, probably, attributed to fully unofficial activities that are even harder to assess. Below is the rating that results from our inquiry.

Comparative analysis of different tax evasion/avoidance avenues in Ukraine by their fiscal effects

| Tunrover, appr. (bn UAH annually) | Conditional budget revenue losses (bn UAH annually) | |

| Aggressive tax planning (tax havens) | 260-320 | 50-65 |

| Industrialized “tax laundries” | 40-50 | 12-15 |

| VAT fraud | 50-60 | 10-12 |

| Import underinvoicing, smuggling | 80-230 | 25-70 |

| Counterfeit, illegal production | 10 | |

| Profit shedding through pseudo sole proprietors on STS | 15-16 | до 2,5 |

| pseudo sole proprietors on STS instead of employment | 10 | 2,5 – 5 |

| Underreporting of sales by sole proprietors on STS | 18 | 1- 1.5 |

#1: Tax havens

Large firms avoid taxes using “tax havens” all over the World, and Ukraine is not an exemption. However, due to abnormally large concentration of property (according to the latest available estimation 18 billionaires together hold about 40% of the country’s GDP in 2014) combined with “oligarchic” nature of their wealth, Ukraine appeared among the World’s leaders in “Illicit capital outflows”, as estimated by the Global Financial Integrity using the World trade statistics: they constituted from 3% to 10% for 2005-2014.

Adjusting the data used by the authors of that report to present time proportionally to change in total trade volumes, and adding 65 bn. UAH paid in 2016th as an interest to affiliated companies (mostly located at tax havens) or at abnormally high rates, we ended up with estimation of total capital outflows of roughly 10% of the GDP. It is a shocking figure, but it corresponds to the NBU’s data and the recent tax authority’s top official’s statement that almost 3/4 of all export contracts are “indirect” – that is, include an offshore intermediary. Given that exports constitute about a half of the official GDP, and some outflows are associated with imports too, this figure becomes looking quite realistic. It means, in turn, that some 2% of the GDP are conditional budget losses associated with profits concealed in tax havens – thereby the potential corporate income tax’s (CIT) revenues are almost halved.

Adjusting the data used by the authors of that report to present time proportionally to change in total trade volumes, and adding 65 bn. UAH paid in 2016th as an interest to affiliated companies (mostly located at tax havens) or at abnormally high rates, we ended up with estimation of total capital outflows of roughly 10% of the GDP.

The remedies are mostly known and already under way, although few of them implemented, and so far none works as it should. First of all, the CIT should be replaced (for many good reasons explained in more detail here) by the tax on capital withdrawals also knowт as “capital exit tax”. The draft law on it stipulates strong and strict measures that make the main channels for illicit outflows direct subject to taxation at higher rate than normal dividends. At the same time, it leaves few reasons to audit the most of ordinary firms not involved in the operations bearing high risk of illicit outflows. This gives the tax authorities (after reforming) a possibility to focus on the largest avenues of tax avoidance, such as transfer pricing where the control is currently non-performing.

On top of this, Ukraine joined the BEPS plan prepared by the OECD that will also facilitate fighting aggressive tax planning. Although, it’s measures should be implemented with great caution, as some of them include highly discretional instruments that should not be given to Ukrainian authorities due to high risk of abuses. Of course, tax avoidance is not the only reason for using offshore jurisdictions – there are important legal advantages too, but the proposed measures should not affect normal relationships between foreign investors of any kind, and their daughter companies in Ukraine.

#2 (shared): customs, illegal production and the “industry of tax evasion”

There are three channels of tax evasion that share the second place, each of them being estimated only very roughly at 1% of the GDP or up to three times more: the customs (smuggling and “grey” imports), the industry of tax evasion, and illegal production – mostly of the alcohol and agriculture production.

Customs abuses can be indirectly assessed by the same trade statistics that seems to suggest surprisingly dramatic improvements that happened after the Revolution of Dignity: looks like these abuses collapsed three times (see the main study for details), from about 10 bn. USD in 2013 to 3.3 bn. USD in 2016, respectively the losses fell to about 1% of the GDP. It can be partly explained by elimination of especially impudent operations, like smuggling of the car fuels in huge amounts by the companies owned by Sergey Kurchenko, one of the Yanukovich’s “wallets”. But at least partly such a dramatic drop in official figures can be attributed to a number of other factors as well; so as of now one cannot be confident if this drop occurred in deed at that great scale. Maybe, at least some part of the corresponding flows of goods just got totally illegal or appeared “below the radars” of trade statistics due to proliferation of more sophisticated schemes.

Similarly, the “industrial” tax evasion that seemed to be the largest tax evasion channel four years ago probably contracted many times after the escape of Yanukovich (who made it semi-legal and became its main beneficiary), and later on – introducing of the VAT accounts that largely complicated any kinds of the VAT fraud, although so far failed to eliminate it completely. Arguably, this “industry” is now responsible for also about 1% of the GDP as lost budget revenues, but there is no hard data to verify scattered numbers from time to time provided by some officials – in deed, the amount involved may be higher.

This “industry” is now responsible for also about 1% of the GDP as lost budget revenues, but there is no hard data to verify scattered numbers from time to time provided by some officials – in deed, the amount involved may be higher.

Unregistered (thereby, untaxed) production of hard drinks is estimated by the market’s experts as almost equal to the legal one, thereby about 10 bn. UAH are underpaid as excise tax. Such drinks are being manufactured everywhere – from the underground home moonshine shops to modern official factories that work an additional shift without an excise tax. Unofficial agricultural crops are planted at the land that is not officially rented – which constitute as much as 40% of all arable lands. By the estimations of the All-Ukrainian Agriculture Council, the budget revenues loss can be as high as 40 bn. UAH, although a conservative estimation is rather 16 bn. UAH.

And, as long as the land is concerned, one should add 5-10 bn. UAH that are undercollected as a land tax: 5 bn. – as MinFin’s estimation of the losses from unduly collection, and up to the same amount of tax privileges granted to different, mostly large, companies by the discretion of local authorities. A more robust review of these privileges is still pending.

The measures against these kinds of evasion involve mostly institutional reforms of the customs service and tax authorities, especially the tax police.

The customs reform as well as the SFS reform prepared by the MinFin and already adapted by the CabMin were abruptly cancelled by the PM Volodymyr Groysman at the beginning of 2018. This episode demonstrates how long way to get them through can be. Аnother sad example on related issue is the Financial Investigations Service that should replace totally corrupt tax police already (occasionally) outlawed a year before and still debated. The main stumbling stone in all of these reforms is how far they should go in replacement of old stuff infected with Nikolay Azarov’s corporate culture of corruption, extortion, repressions and hostility to business.

Recently some restrictions were imposed on citizens that work as “ants” carrying maximally officially allowed amount of goods cross the border daily; or receiving dozens of valuable parcels with such goods.

However, without the customs service reform it can result in rather reshuffling then significant contraction of smuggling. The property/land tax should be modified using modern approaches, its collection improved by a number of technical (e.g. establishing instant correspondence between the data bases) and economic (e.g. using potential property tax revenues instead of actual in the calculations of transfers to local authorities) measures.

The property/land tax should be modified using modern approaches, its collection improved by a number of technical (e.g. establishing instant correspondence between the data bases) and economic (e.g. using potential property tax revenues instead of actual in the calculations of transfers to local authorities) measures.

Note that all these issues (but land tax) involve some other violations too: the smuggled or illegally produced goods should be then sold, while the money received from “industrial” tax-evasion firms are further used for paying the envelope wages and bribes. This gives some experts a reason to argue that the problems can be better solved if addressed at some other point of the chain – for instance, at the end selling point for goods, or at the firms paying envelope wages. This is probably true in respect to bribes, since if they are not needed any more, then there is no demand for “black cash” for this very purpose. Envelope wages can be, indeed, fought only by further cuts in payroll tax (that should be eliminated as such) and personal income taxes – the latter should not exceed 10%, just as the tax on capital withdrawals. However, none of this can stop the VAT fraud.

Besides, it is much easier to catch illegal traffic of goods or money at some innumerous focal points rather than try to control hundreds of thousands small vendors, or millions of employees. In case of smuggled or illegally produced goods the control of end sales does not work at all, since the same “tax evasion industry” handily provides such goods with fake documents (for instance, issued by a short-living fake company) – just as it works now, particularly with alcohol that is, formally, subject to such control. Note that upper estimations of the volumes imported illegally or with violations exceed total reported turnover of all small retailers subject to STS. Last but not least, it is much easier to control for corruption at the customs – with instant video surveillance, scanners images, and online documentation that can be made available for supervising bodies 24/7 – then at the inspections of end sales points.

#3: abuses of simplified taxation

Finally goes the STS that is routinely claimed as, allegedly, the main component of Ukrainian shadow economy and, allegedly, “the inner off-shore”. In fact, due to our estimations, all of the violations associated with the STS are responsible for 4.2 – 9.5 bn. UAH (0.2-0.4% of the GDP) of fiscal losses – which is less than cost of unnecessary accounting that these entities should have done without the STS, not to mention the other problems that it solves. This figure does not include, however, illegally produced or imported goods that are being sold through this channel – for good reason that while such goods are already available at the market, they will be (and actually are) sold in different ways, by large – with fake documents, as described above. So, the STS here is not a cause, just a disposable instrument.

There are, however, some real issues with it too.

About 2.5-5 bn. UAH could have been paid, should all of the sole proprietors that are, in fact, employees (by a number of criteria) pay their PIT and payroll taxes, instead of 5% unified tax + fixed social contribution they pay now.

However, this is exactly the case when the caution about conditionality of “revenue losses” applies in full: the employees being paid in this way are not the ordinary workers, but highly paid (and highly skilled) specialists, mainly in the IT industry. Therefore, they have a choice on whether to stay in Ukraine, or find some other place on the Globe where they will get better state services for the taxes they paid. In reality these specialists emigrate en masse even now, in spite of such a lucrative taxation. Or, if their employers try to charge higher prices of their customers in order to pay more in taxes, they will simply lose fierce global competition and fail to create these workplaces at all – with exactly the same outcomes. All of this means that should such kind of violations be effectively fought few of these specialists will stay in Ukraine so the Treasury hardly recovers even current revenues from this category of taxpayers. And, even worse, the country would lose its human capital.

All of this means that should such kind of violations be effectively fought few of these specialists will stay in Ukraine so the Treasury hardly recovers even current revenues from this category of taxpayers. And, even worse, the country would lose its human capital.

For this reason, competitiveness policy considerations suggest not to crash on these abuses too harshly, at least as long as there are much larger ones that can be fought against with much less detrimental consequences. In the future, the real remedy is a dramatic cut in PIT and abolishment of any “labor tax” at all. This can be done quite realistically in a few years by steady but consequent budget cuts along with improvements in tax collection.

The rest of estimations above were made by econometric analysis (with kind and invaluable help of Roman Semko) based on the well-studied fact that in a market economy firms are Pareto-distributed by size. Comparing the real distribution with it’s Pareto-approximation we identified the irregularities that can be interpreted as manifestations of certain kinds of violations.

Mainly, the STS taxpayers subject to lump-sum taxation have no other motives for underreporting of their revenues but actual violation of the turnover’s upper limit eligible for the corresponding STS’s group.

The violators are likely to report some amounts close but not exceeding this upper limit, therefore one should expect abnormally high numbers of entities reporting such amounts. And this is exactly what we observe among the entities that do not use cash registers – just with a reservation that from the mid-2015 the entrepreneurs with turnovers over 1 mn. UAH were obliged to use them, which incurs substantial fixed costs and headache. For this reason, starting with that year we see a huge irregularity before 1 mn. UAH, and just a small one – before the upper limit.

The violators are likely to report some amounts close but not exceeding this upper limit, therefore one should expect abnormally high numbers of entities reporting such amounts.

Nevertheless, econometric techniques allow us to restore a real picture, as it probably should look without these irregularities. In such a way we can estimate how many entrepreneurs actually breached the rules by underreporting their incomes, and how many of them exceeded the limit; and assess the respective amounts involved. Although the latter are quite high – more than 50 bn. UAH – the most of them have no fiscal effect, since the respective entities just avoided using the cash registers, but not actually exceeded the limit. Only about 25 bn. were earned by those who indeed exceeded and should have been switch to 3-d tier of the STS to pay 5% of their turnover instead of lump-sum. Which, in turn, means that revenue losses were about 1 bn., and hardly could exceed 1.5 bn.

The 3rd group also demonstrates such irregularity, although much lesser in scale (about 3 thousands of entities, 15 bn. UAH) but much harder to interpret. These could be some larger businesses that just underreport their incomes, as in previous case, but also the entities that deliberately keep their operations within the limit in order to avoid exposure to the hardships of general taxation system, primarily – permanent “talks” with tax authorities. Of them, one part can be just law-abiding business entities; another – those larger ones, who split apart in order to formally keep within the law; and yet another one can represent fake entrepreneurs whose “business” is helping the larger firms in tax evasion by receiving from them the payments – allegedly, for some hardly tangible services – and paying back cash with some minor commissions, almost like the larger “industrial evasion centers” do, but without a possibility to avoid VAT, and at much higher transaction costs. More detailed data are needed to distinguish between the latter case and two former ones hardly dispensable from each other. Assuming that average share of sole proprietors – providers of “hardly tangible” services that, at the same time, have no employees, holds at this part of distribution too, we end up with estimations of fiscal effect that vary from 0.7 bn. in case these fake entrepreneurs are used for profit shading and estimation is taken at the lower bound, to 3 bn. in case of an upper bound, and envelop wages. However, this assumption is not well-grounded, it is just the best we can do before the SFS will be so kind to provide more detailed data upon the request sent half a year ago.

The 1st group does not add much to this picture – it is small while the barrier between it and the 2nd one is not significant. Sole proprietors that use cash registers are rather innumerous but demonstrate even larger (in relative terms) irregularities than the ones who do not. Most probably, this is due to the fact that they, in deed, mostly represent large shops artificially divided into numerous individual pseudo-entrepreneurs. However, their overall fiscal effect is rather minor and uncertain.

Conclusions and implications

The main conclusion of the rating presented above just reinforces the one made more than two years ago: in spite of their high visibility, small but mass violations associated with simplified taxation play minor role, almost exactly proportional to the share of STS taxpayers in the whole private sector. Their total conditional fiscal effect is many times less than the one of aggressive tax planning alone – and it is indeed highly conditional, due to high elasticity and serious side effects of possible crackdowns on the STS. Comparing to the situation few years ago, the “tax-evasion industry” seem to have contracted a few times, probably due to anti-fraud measures in the VAT administration, and, possibly, also due to some de-shadowing of the wages induced by the payroll tax’s cut. Therefore, if then this was the main component of the shadow economy, now it shares the second place with custom violations (also likely shrunk by large), while aggressive planning involving tax havens came to the first place.

The main conclusion of the rating presented above just reinforces the one made more than two years ago: in spite of their high visibility, small but mass violations associated with simplified taxation play minor role, almost exactly proportional to the share of STS taxpayers in the whole private sector.

The main implication that follows also reiterates the one of the first article: sequence matters. Namely, to the extent fiscal goals are concerned, for all reasons – managerial, economic, socio-political, and organizational – the best way to proceed is to focus each time on the largest avenues of tax evasion/avoidance amending these priorities according to changes in the real-life situation. From this perspective, tools that are able to reduce tax avoidance/evasion by large are already there or under work. First of all, according to the priorities stemming from presented rating, these are measures against aggressive tax planning: the tax on withdrawn capital, BEPS, institutional reforms of the SFS and customs service, the FIS replacing incapable and corrupt tax police. Then go completion of the VAT administration reform, and – last but not least – further dramatic reduction in the size of the state that should give fiscal space for major cuts in the income taxes and abolishment of the labor tax. We already have success stories with payroll tax’s cuts and the VAT administration’s reform that we can build on, but there is still quite a long way ahead.

Attention

The author doesn`t work for, consult to, own shares in or receive funding from any company or organization that would benefit from this article, and have no relevant affiliations