Last year, Ukrainian metallurgy faced numerous challenges resulting in a three-fold decline in production. These challenges included factory shutdowns and occupations, electricity and working capital shortages, decreased demand, and complex logistics. The last factor is probably the most important. With the majority of steel products being exported by sea (80%), the blockade of Black Sea ports not only caused a three-fold reduction in export volumes but also resulted in the loss of foreign markets. Simultaneously, imports have become increasingly significant for domestic consumption due to product shortages, as the factories in Mariupol were the sole producers in Ukraine.

This year, Ukrainian producers are forced to build their production and sales strategies taking into account both the blocked ports and the global market conditions, which are not too optimistic. Moreover, companies are facing new challenges, such as water shortages due to terrorist attacks by the aggressor country.

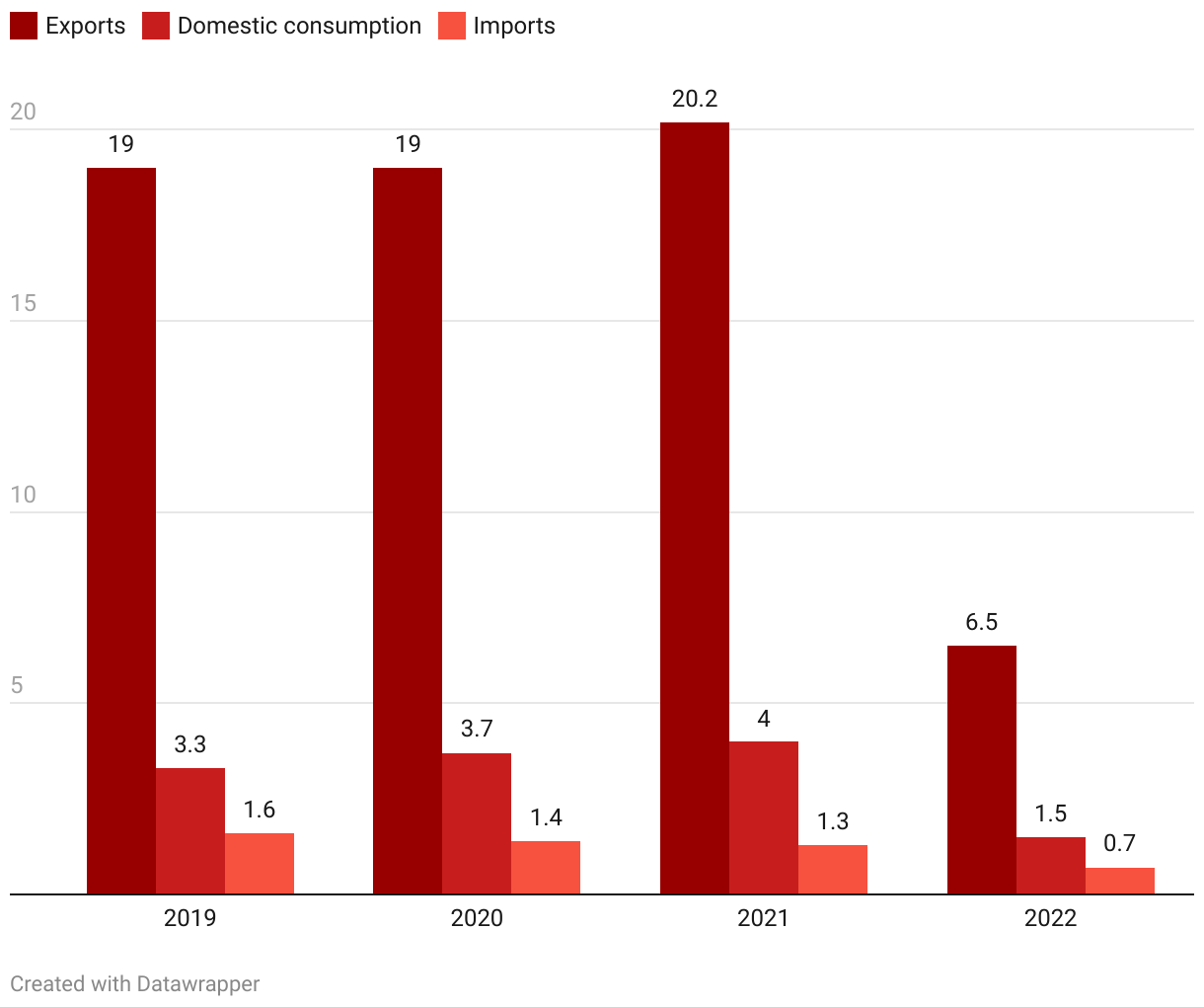

The full-scale invasion by russia profoundly impacted Ukraine’s foreign trade activity, causing a decline in key indicators (Figure 1). The export of steel products, typically amounting to several tens of million tons, experienced a three-fold decrease. Nevertheless, the majority, approximately 80%, of the products manufactured by Ukrainian metallurgists continued to be exported as before.

Figure 1. Export, import, and consumption of steel products in Ukraine, million tonnes

Source: Ukrmetalurgprom, State Customs Service of Ukraine data, and expert assessments.

This article’s analysis of foreign trade considers goods of group 72 (“Iron and steel”) and commodity items 7301-7306 of group 73 (“Articles of iron and steel”) of the Commodity Nomenclature of Foreign Economic Activity (CN FEA) to be metal products or steel. Domestic consumption does not include raw materials (pig iron, scrap, ferroalloys), with data for 2022 being expert assessments.

Prior to the full-scale invasion, Ukraine’s imports of steel products surpassed 1.3 million tonnes, accounting for approximately a quarter of the apparent consumption (which includes both production and imports but excludes exports) in the domestic market. However, last year, the volume of imports decreased by half, yet its proportion in domestic consumption rose to one-third.

The decline in imports and domestic consumption can be attributed to two primary factors: constrained logistics and reduced demand for rolled steel due to a slowdown in economic activity caused by the occupation of territories, active hostilities, russian attacks on critical infrastructure facilities, and population migration abroad.

Export of steel products from Ukraine

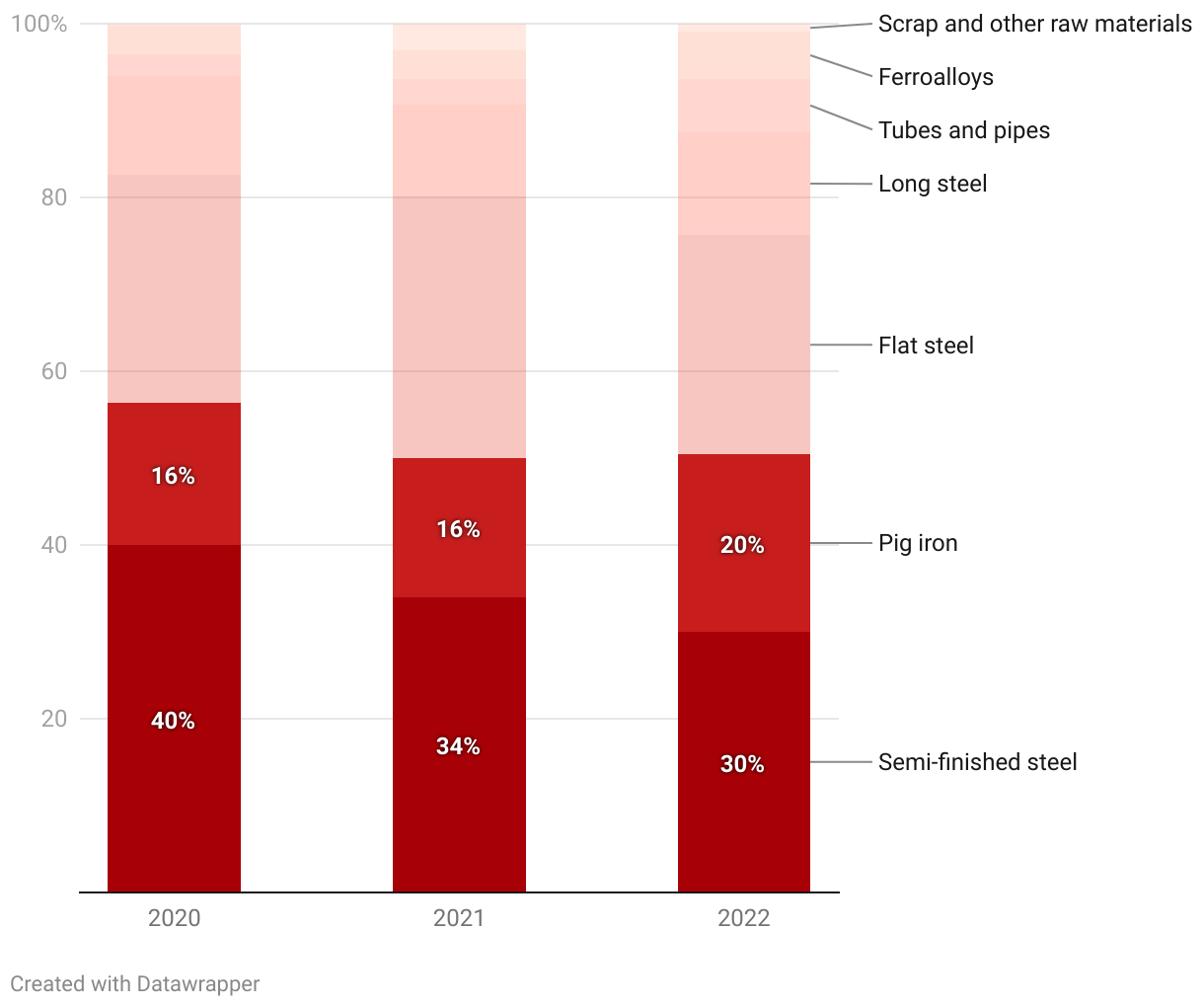

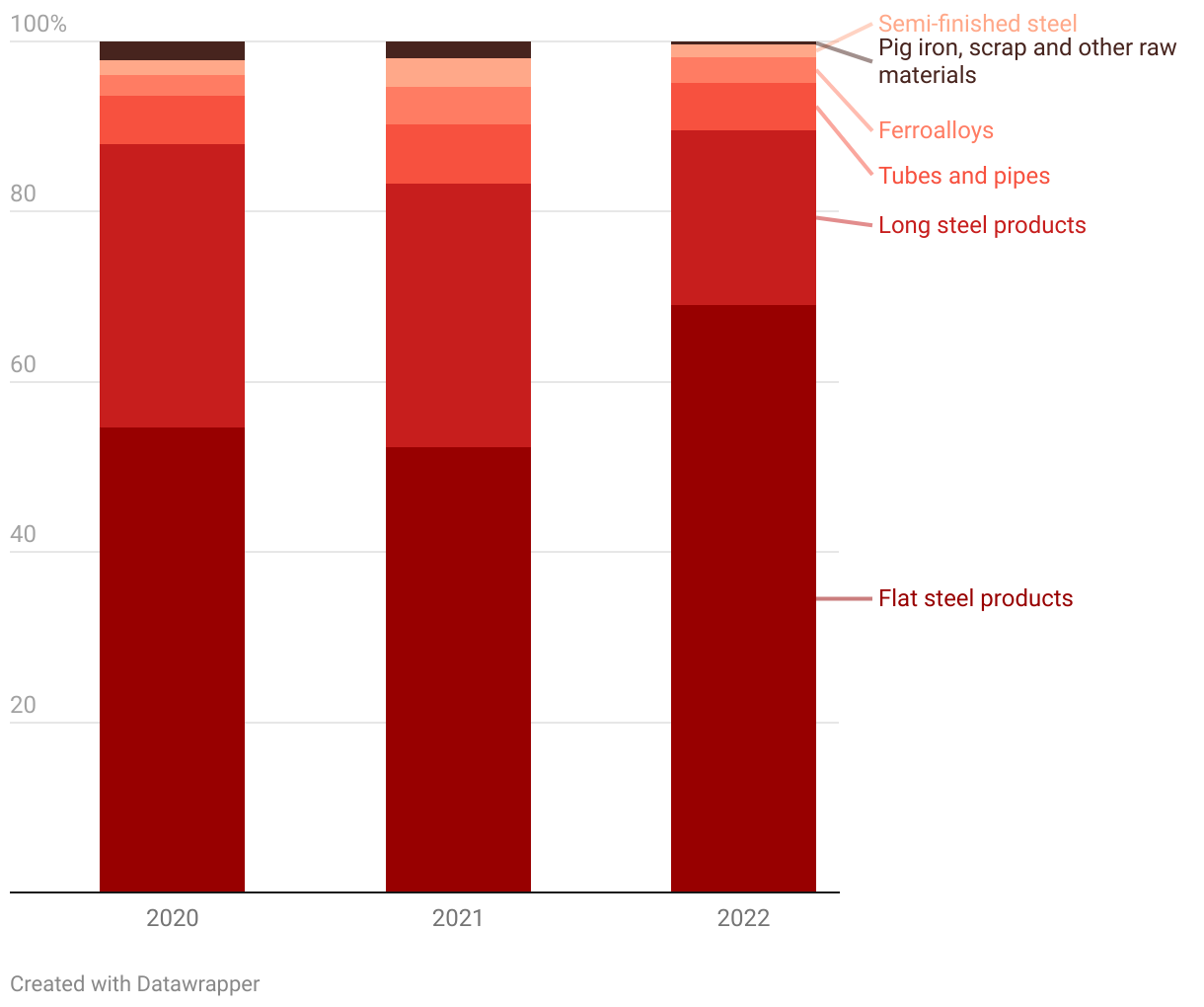

Semi-finished products and pig iron (as shown in Figure 2) constitute approximately half of the product structure in the export of metal products. These products are generally less lucrative compared to finished rolled steel, which finds applications in various sectors such as construction, automobile and machine building, the oil and gas industry, and more.

Before the full-scale invasion, manufacturers were motivated by supplying semi-finished products to their own assets abroad and responding to market conditions. However, last year, the situation shifted to a “survival” mode, where companies focused on supplying the products they were capable of producing and shipping. For instance, during periods of power outages in the fall, mills reduced the production of rolled steel, which is energy-intensive, and instead prioritized smelting pig iron, which relies more on gas.

A substantial portion of the supply consists of the export of flat-rolled products. However, the volumes of these exports have declined because the main producers of such products are the Metinvest Group’s plants in Mariupol, which are currently occupied.

Figure 2. Commodity structure of exports of steel products of Ukraine, %

Source: State Customs Service of Ukraine

Last year, positive changes were observed as well. The suspension of import duties in the USA and the rise in prices for pipe products, which carry a significant added value, contributed to an increase in their share within Ukraine’s exports from 3% to 6%.

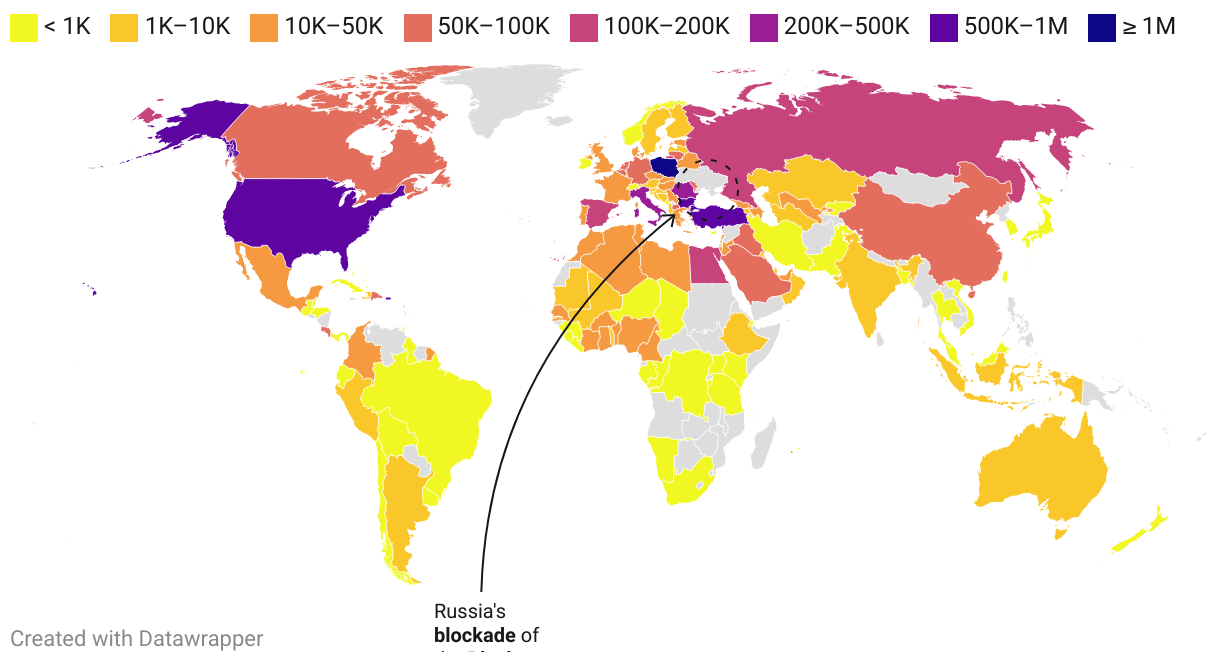

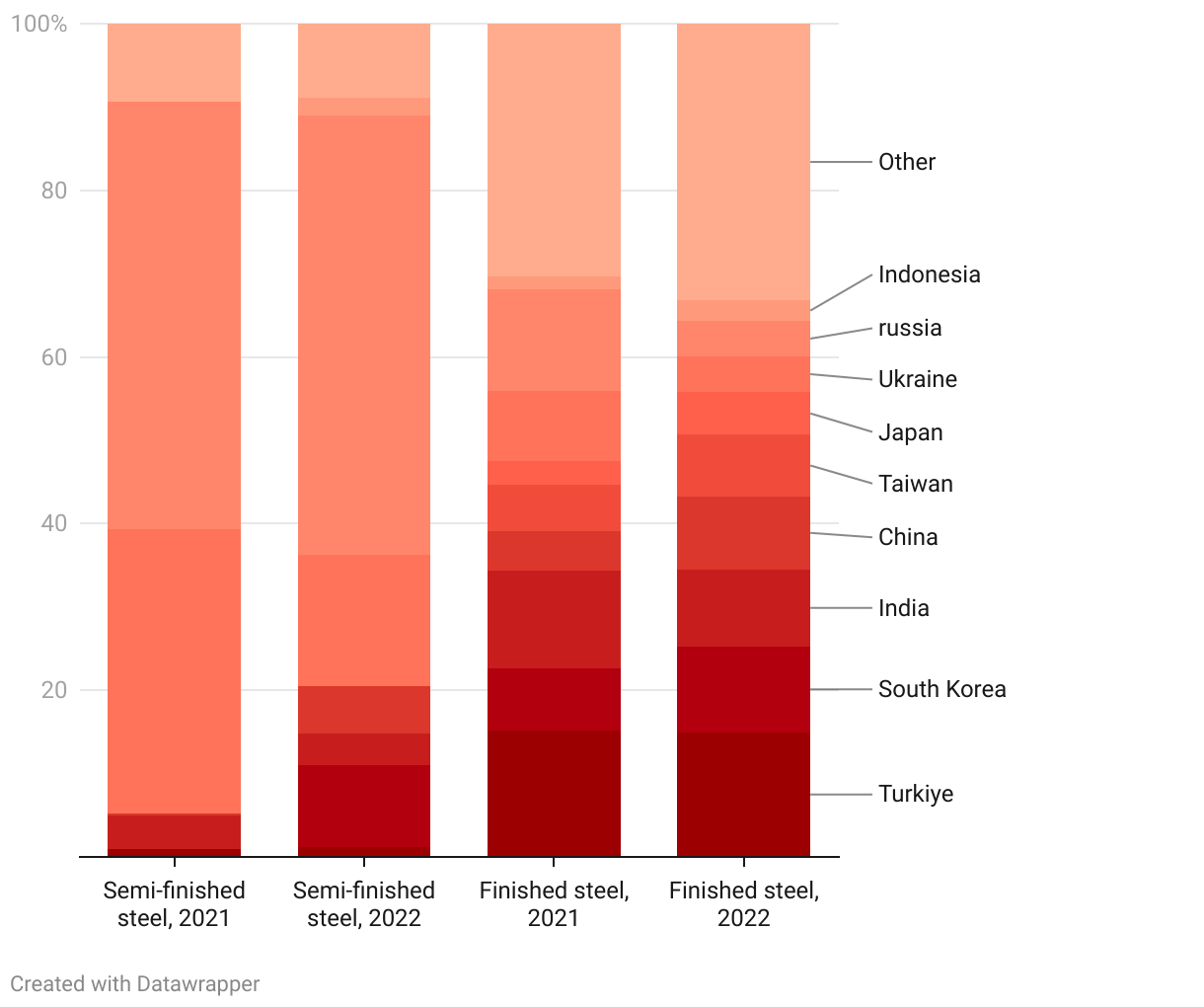

Ukraine’s export of steel products extends to nearly all continents worldwide (as depicted in Figure 3). The companies operating in “normal” mode during the first two months of 2022 (accounting for 43% of the total volume of steel products for the year) helped maintain the existing geographical presence of Ukrainian manufacturers by the end of the year. However, there was a noticeable decline in the number of countries receiving Ukrainian exports, decreasing from 98 in the first quarter of 2022 to only 62 in the fourth quarter.

Figure 3. Geography of exports of Ukrainian steel products in 2022, tonnes

Source: International Trade Center

Note. Almost the entire volume of exports to russia was sent in the first quarter of 2022, with a small cargo shipped in September. Officially, exports to the russian federation were banned at the end of September 2022.

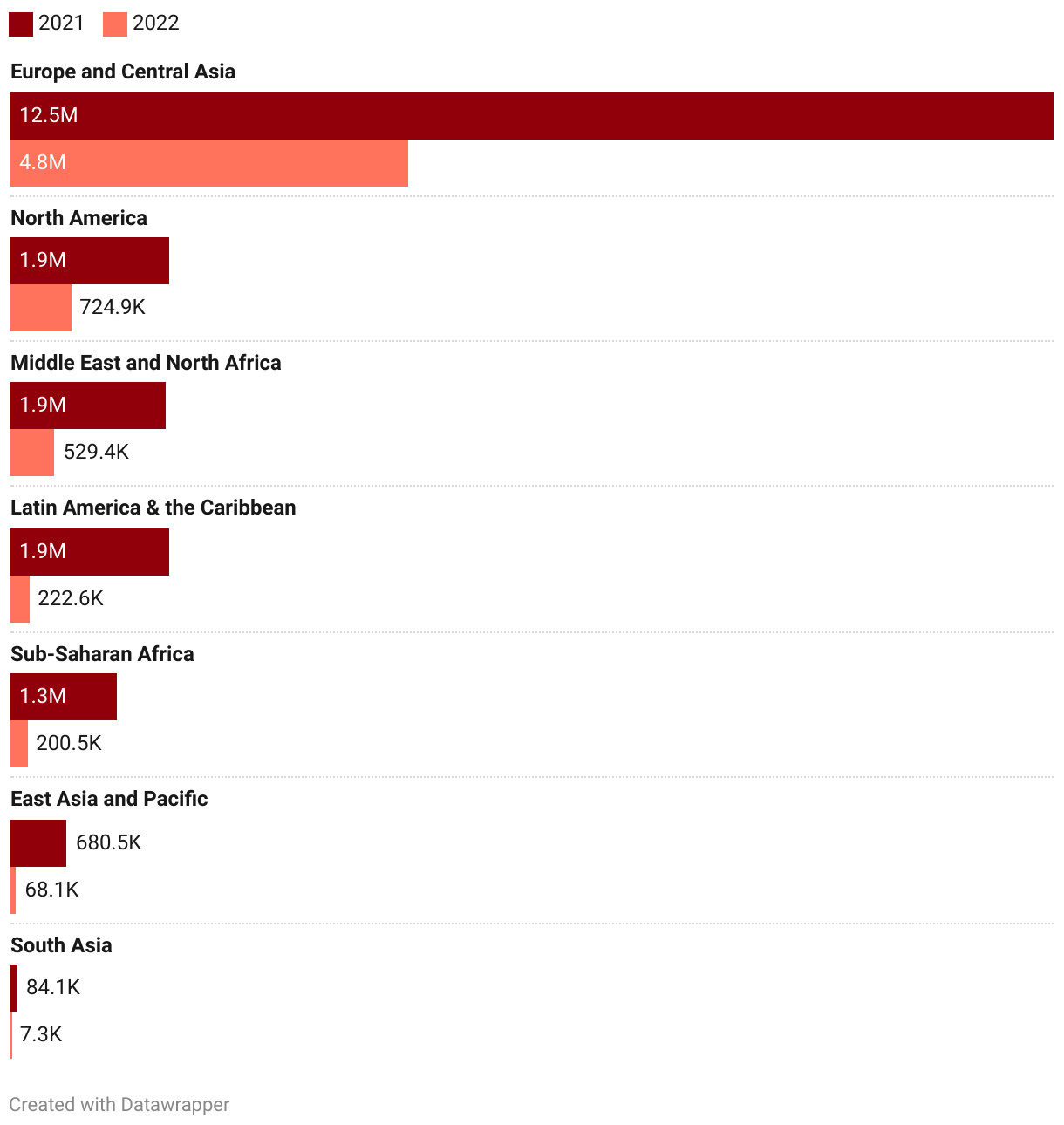

The decrease in volumes of metal product exports had an impact on all sales regions, spanning from Europe to the distant Pacific region (as depicted in Figure 4). The extent of the decline varied based on the distance the cargo had to traverse to reach the buyers, considering the logistical challenges involved. As a result, the presence in remote destinations nearly vanished due to these circumstances.

Figure 4. Regional structure of export of Ukrainian steel products, tonnes

Source: International Trade Center

The regional distribution of countries has been conducted according to the classification of the World Bank.

Specifically, exports to Southeast Asia and Oceania experienced a tenfold decline, while exports to Latin America dropped by 8.5 times, given the disrupting traditional transportation routes. Furthermore, supplies to African countries located south of the Sahara Desert witnessed a decrease of over sixfold.

The situation in the Middle East and North Africa differed somewhat as exports to this region experienced a decline of 3.5 times against the backdrop of the blocked traffic through the Black Sea and the absence of Mariupol mills among the suppliers. Ukraine exported 79% of last year’s volume to this region during the first quarter.

In terms of export volumes, North America stands as the second-largest destination for Ukrainian exports. Last year, sales to this market experienced a relatively smaller decrease of 2.6 times. Similar challenges were encountered, including logistical limitations, the absence of Mariupol suppliers, and reduced production in territories under Ukrainian control. However, Ukrainian companies partially adjusted their shipping routes by diverting exports from Black Sea ports to European ports. This adaptation allowed for an increase in the export of some goods. For instance, Ukrainian manufacturers of seamless pipes witnessed a 21% year-on-year increase in their exports to the USA thanks to the suspension of import duties.

Despite the decrease in supply volumes by 2.6 times, Europe and Central Asia continued to be the primary consumers of Ukrainian steel products. Remarkably, their share expanded to 72% since Ukrainian manufacturers redirectied trade flows through land and river transportation to neighboring countries.

The European Union emerged as the primary destination for Ukrainian exports, with its share in the total volume of Ukrainian steel exports rising from 35% in 2021 to 57% in 2022. In the second half of last year, this share further increased to 90%. Several factors contributed to this shift. Firstly, the blockade of the Black Sea compelled Ukrainian manufacturers to redirect trade flows towards neighboring countries, particularly Poland (which saw a 7% increase in exports from Ukraine). Secondly, the European Commission suspended trade protection measures on Ukrainian products. Lastly, exports to russia, which was one of Ukraine’s top five largest trade partners, were minimized during this period.

The global metallurgical industry has been grappling with excess production capacity in recent years, primarily due to establishing new production facilities in Asia and the Middle East. Consequently, the disposal of Ukrainian volumes does not pose a critical problem for international consumers, as alternative suppliers can readily replace them.

Partial compensation of Ukrainian volumes occurs through regional trade. Moreover, Asian manufacturers are taking a more prominent role and strengthening their positions in the Middle Eastern and European markets. For instance, in the segment of semi-finished and finished steel products, volumes that were previously supplied by Ukraine and partially by russia have been replaced by Asian producers (as shown in Figure 5). This trend has been ongoing and continues in the current year.

Figure 5. Geographical structure of steel imports in the EU-27, %

While Asia is currently stepping in to replace the volumes previously exported by the damaged Mariupol facilities, it may face challenges in the long run. Several important points should be considered. Firstly, despite the lower production costs, transportation expenses from Asia to Europe need to be taken into account. Secondly, import quotas are in place, limiting the volume of shipments from Asian producers. As a result, they may not be able to exceed these established quotas. Lastly, the European Union is increasingly moving towards green metallurgy.

Considering Europe’s decarbonization targets, it is expected to be extremely challenging for most Asian producers, such as China and India, to achieve carbon neutrality even in the medium term. In contrast, Ukraine has an opportunity to “rebuild better” after the war and transition to a new green technological level. This shift aligns with the goals of sustainable development, as emphasized by experts and steelmakers.

Presently, the primary diplomatic efforts are focused on including metallurgical products in the grain agreement and enhancing the transportation infrastructure in Ukraine and Europe. This involves initiatives to improve railways, transshipment hubs, checkpoints, and port infrastructure.

Import to Ukraine

Most imports of steel products to Ukraine are made up of goods that are either not produced in the domestic market or do not meet the quality/pricing requirements of consumers. Primarily, this includes flat-rolled products: its share in imports previously exceeded 50%, and in 2022, it increased to 69% (Figure 6). Before the invasion, mainly coated flat-rolled products were imported as the domestic producers could not fully meet the demand. The need for hot-rolled flat products, which used to be produced by Mariupol-based plants, also increased, given that Zaporizhstal, the only producer of these products at present, was operating intermittently due to a shortage of electricity. Additionally, the import of products previously solely produced by Azovstal, such as beams and rails, has increased.

Figure 6. Commodity structure of steel imports to Ukraine, %

Source: State Customs Service of Ukraine

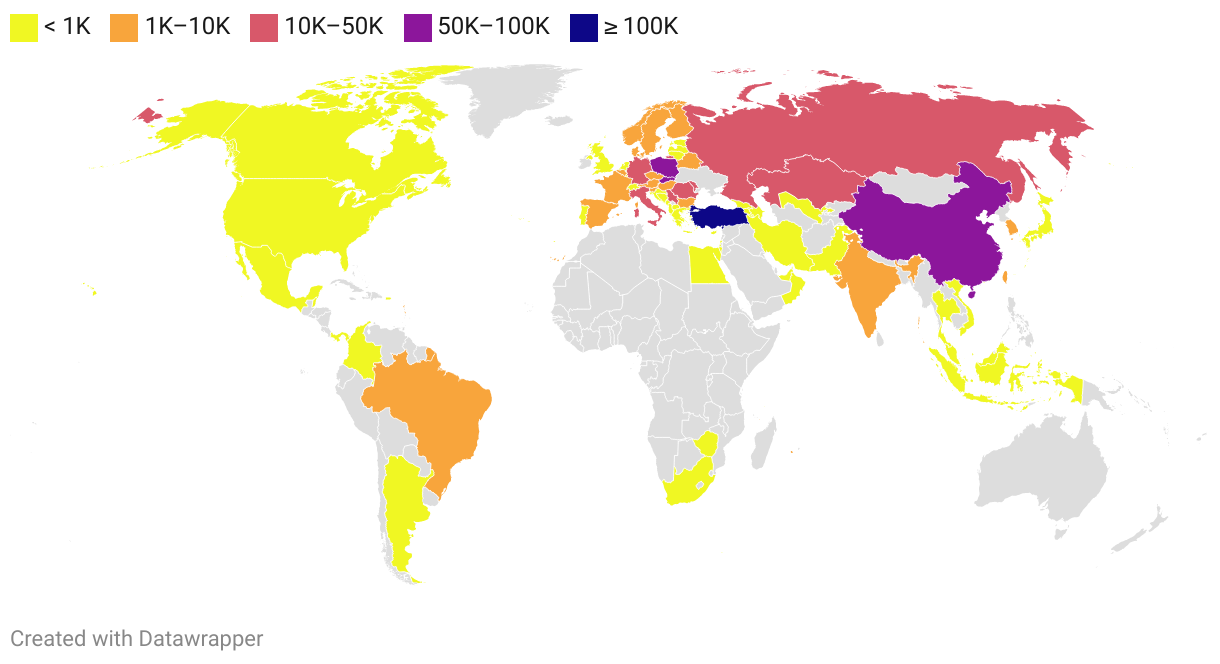

Until last year, the major steel exporters to Ukraine were russia, China, and Turkiye, accounting for over half of the import volumes. However, for obvious reasons, russia lost its position when an import embargo was imposed in April 2022. Imports from Turkiye also decreased by 20%. Nevertheless, Turkish producers emerged as the primary source of rolled steel for Ukraine in 2022, and by the fourth quarter, import volumes reached pre-invasion levels. Purchases from China experienced a significant decline of 61% due to logistical challenges. Like Turkiye, China meets Ukraine’s demand for flat rolled products, particularly coated rolled products used in construction (e.g., corrugated board), automobile manufacturing, and household appliances. However, the inflow of Chinese coated rolled products may further decrease if new anti-dumping duties on this product are established in Ukraine.

Figure 7. Geography of steel product imports to Ukraine in 2022, tonnes

Source: International Trade Center

Similar to the export segment, European countries have played a supportive role in supplying steel products to Ukraine by increasing trade flows. Slovakia has emerged as the third-largest exporter to Ukraine, while the volume of supplies from Romania has nearly quadrupled. Notably, Romania has been able to establish the supply of scarce products, specifically flat-rolled products, to Ukraine.

Where does the situation stand this year?

There are currently no official detailed statistics for the first five months of 2023, but the main trends can be seen.

Firstly, the stabilization of the electricity supply situation in February resulted in increased production volumes for Ukrainian manufacturers. Thus, in March, crude steel steel production increased by almost a quarter compared to February, while rolled steel production grew by 30%, according to the according to Ukrmetallurgprom. The upward trend continued in April and May.

Overall, both for the first quarter and the first five months of the year, operating results remain significantly lower than last year’s volumes, given the high comparison base of January-February 2022, but Ukraine has increased production compared to the last quarter of last year.

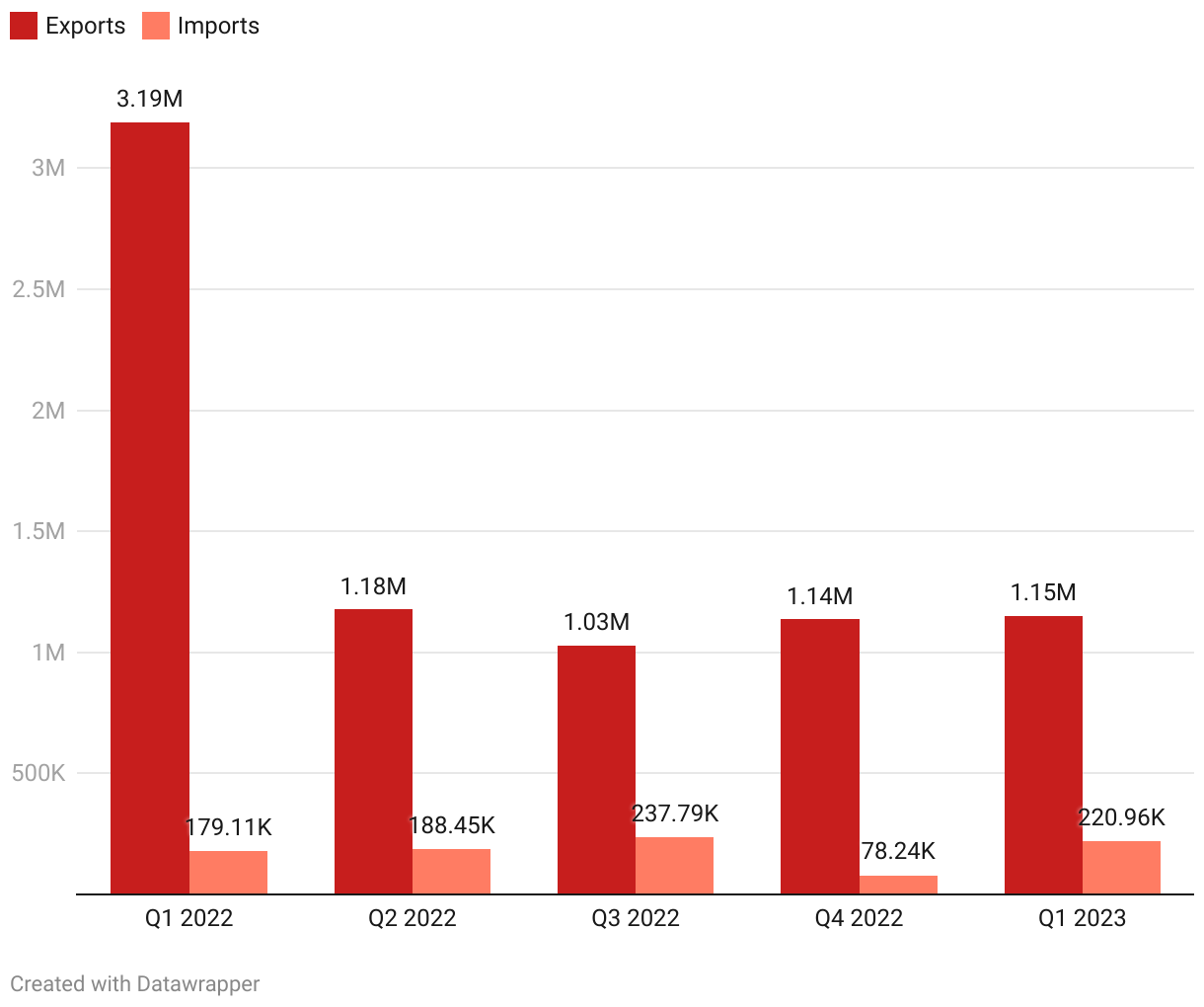

Secondly, steel imports also increased, given the increased consumption in the domestic market (Figure 7) ahead of the construction season and due to disruptions in the operation of local steelmaking companies in winter.

Figure 8. Quarterly volumes of Ukrainian exports and imports of steel products, tonnes

Thirdly, the reorientation of all export goods to the western border, primarily agricultural products and iron and steel, has led to significant competition among exporters and increased queues at the borders due to limited capacity.

In such a situation, a temporary restriction on grain imports from Ukraine to certain EU countries could help boost exports of mining and steel products by reducing congestion at the borders and provided that the price situation on the iron ore and steel products markets is favorable. In addition, railroad transportation is also declining due to the unstable operation of the grain corridor. According to April’s operational data, export transportation of goods by rail decreased by 8% compared to March due to a decrease in grain shipments (-15%). However, export transportation of metal products increased by 16%. In May, export rail transportation of ferrous metal products continued to grow to almost 0.5 million tonnes, while grain transportation almost halved.

At the same time, the terrorist attack on the Kakhovka hydroelectric power plant is becoming a new challenge for the Ukrainian steel industry. For example, Kryvyi Rih’s water supply was 70% dependent on the Kakhovka reservoir, so ArcelorMittal Kryvyi Rih, the largest steel producer in Ukraine, stopped steelmaking and rolled steel production to minimize water consumption. At the time of publication, the company has not resumed production. Nikopol Ferroalloy Plant was also forced to cut production.

Conclusions

The data shows not only a reduction in the volume of Ukrainian steel products exported abroad in 2022, but also a forced reduction in the markets of presence. As steel cannot be shipped through traditional ports such as Pivdennyi, Mariupol, Odesa, Mykolaiv, etc., companies have shifted to using railways, Danube river ports, and European seaports, and focused on the closest possible markets – European countries. As a result, producers have reduced cooperation with regions with longer transportation routes.

It is difficult to predict how long Ukrainian producers will be limited in their export opportunities, given the ongoing war and the need for additional financial resources and time to develop transport infrastructure. This is in addition to the issue of rebuilding assets in the temporarily occupied territories. Ukraine plans to establish new joint railroad checkpoints on the border with the EU in 2023-2024 and to develop the railroad by repairing, modernizing, and laying new tracks. In turn, European partners, such as Poland, through whose ports Ukrainian mining and metals products were shipped, plan to expand the capacity of the Gdansk port by 50% by 2025.

In addition, the following factors are worth paying attention to. The shift to shipping Ukrainian products by rail instead of sea has led to a multiple increase in transportation costs. Consequently, in times of declining steel prices on international markets, high transportation costs make our products less economically attractive, as the share of logistics costs increases. According to industry analysts and the National Bank of Ukraine, iron ore and steel prices will continue to decline in the second and third quarters of this year, which may put pressure on the competitiveness of Ukrainian suppliers.

Moreover, even as new logistics routes are being established, Ukrainian producers are facing weaker demand for steel products in key markets, particularly in Europe, which also limits their plans to increase production. This was stated by Mauro Longobardo, CEO of ArcelorMittal Kryvyi Rih, at the international conference “Onwards and Upwards: Reforming Ukraine During the War” held on May 19 in Kyiv.

In addition, the prospects for increasing steel production in Ukraine may be limited again due to a drop in electricity supply. In particular, there is a risk of electricity shortages in the summer, which may force the industry to either cut back on electricity consumption or import more expensive energy from Europe.

Last but not least, water shortages at enterprises in the Dnipropetrovsk region that rely on the Kakhovka reservoir may become another challenge along with electricity shortages.

As for imports, it will continue to grow and account for an important share of domestic consumption until Ukraine resumes production of deficit goods. Russia has ceased to be the main supplier of steel, being replaced by Turkiye, European countries, and, in some commodities, China.

Attention

The author doesn`t work for, consult to, own shares in or receive funding from any company or organization that would benefit from this article, and have no relevant affiliations